NO.PZ201701230200000306

问题如下:

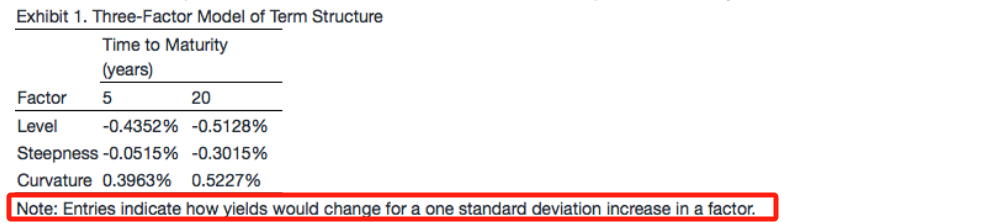

6. Based on Exhibit 1, the results of Analysis 1 should show the yield on the 20-year bond decreasing by:

选项:

A.0.3015%.

B.0.6030%.

C.0.8946%.

解释:

B is correct.

Because the factors in Exhibit 1 have been standardized to have unit standard deviations, a two standard deviation increase in the steepness factor will lead to the yield on the 20-year bond decreasing by 0.6030%, calculated as follows:

Change in 20-year bond yield = -0.3015% ×2 = -0.6030%.

只要是Three-Factor Model of Term Structure 给出这个表就是某个factor变动一个标准差,yield的变化对吗?