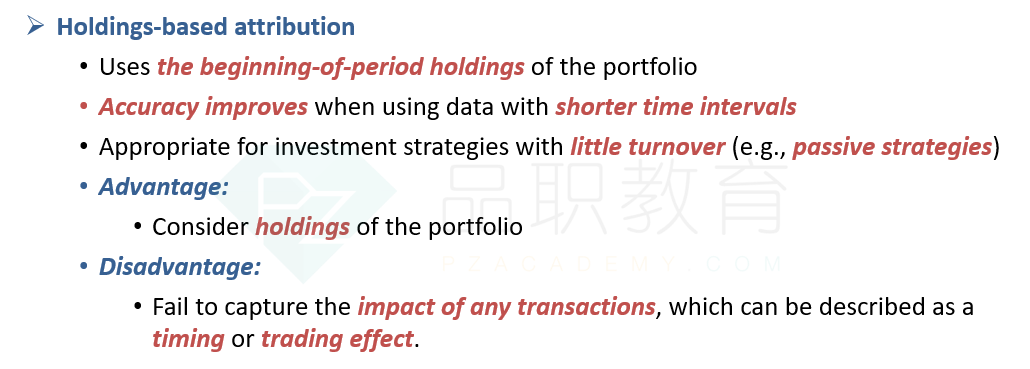

Timmon then asks Richard why holdings-based attribution can generate a residual term between the portfolio performance and benchmark performance. Richard responds that the residual term cannot be explained by an action taken by the fund manager, but it could result from transactions occurring more frequently than the holdings assessments for the fund.

Richard’s answer with respect to holdings-based attribution is best described as:

A.

correct.

B.

incorrect in regard to the fund manager’s action affecting the residual term.

C.

incorrect in regard to the frequency of measuring holdings relative to transactions.

这题解答帮忙解释一下

这个考点在讲义哪个部分提及了?