NO.PZ2020011303000083

问题如下:

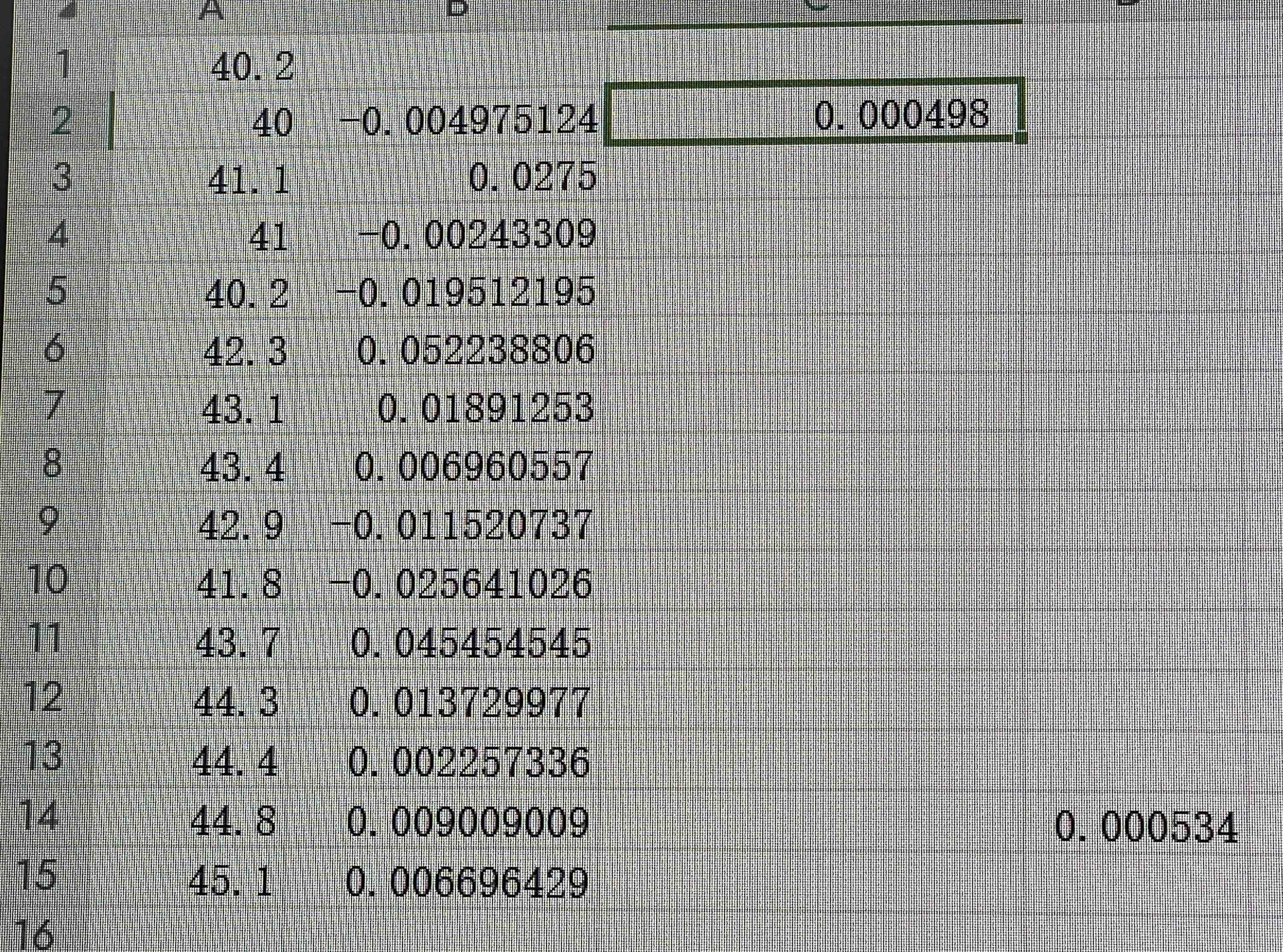

Suppose that the observations on a stock price (in USD) at the close of trading on 15 consecutive days are 40.2, 40.0, 41.1, 41.0, 40.2, 42.3, 43.1, 43.4, 42.9, 41.8, 43.7, 44.3, 44.4, 44.8, and 45.1. Estimate the daily volatility.

解释:

The 14 daily returns are –0.498%, 2.75%, –0.243%, …. The average of the squared returns is 0.000534, and the volatility estimate is the square root of this or 2.31%.

题目问:假设股票价格在接下来的15天里是40.2, 40.0, 41.1, 41.0, 40.2, 42.3, 43.1, 43.4, 42.9, 41.8, 43.7, 44.3, 44.4, 44.8, and 45.1,估计一下每日收益率的波动率。

首先计算每日的收益率=(P1-P0)/P0

然后每一个值求平方,相加取均值之后等于0.000534

开根号之后就是波动率=2.31%

老师好,15天的价格,14个收益率,用excel计算这些收益率的方差是0.000498,不是0.000534,是我哪里算错了吗?