NO.PZ2023052301000046

问题如下:

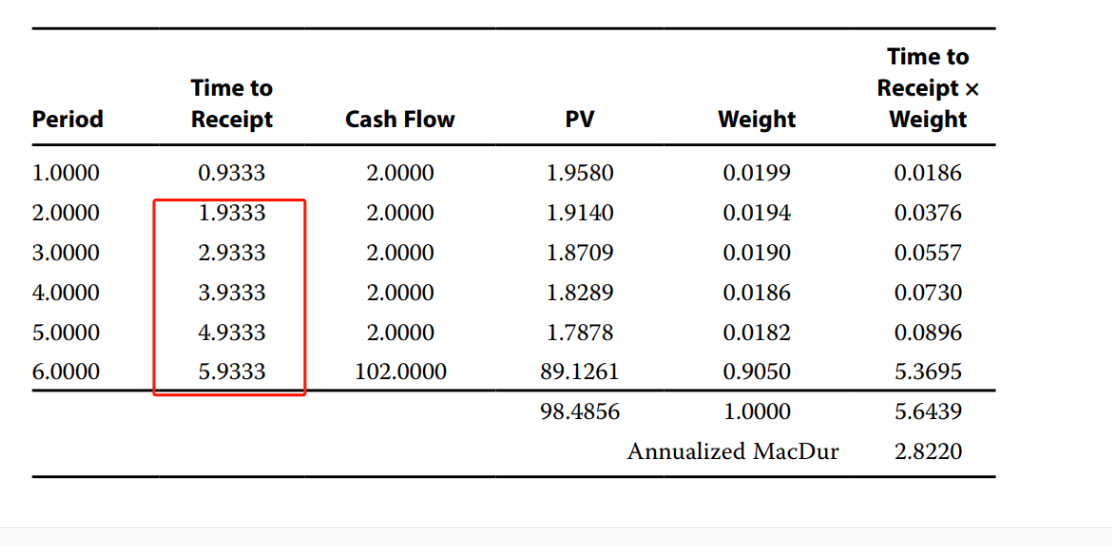

Consider a bond that has three years remaining to maturity, a coupon of 4% paid semiannually, and a yield-to-maturity of 4.60%. Assuming it is 12 days into the first coupon period and a 30/360 basis, the bond’s annualized Macaulay duration is closest to:

选项:

A.1.8764 years.

2.8386 years.

2.8553 years.

解释:

B is correct.

这看不懂怎么后面的period直接加1?能列一下原始的公式么?譬如Priod2 1/1.023的多少次方?