NO.PZ2020011303000068

问题如下:

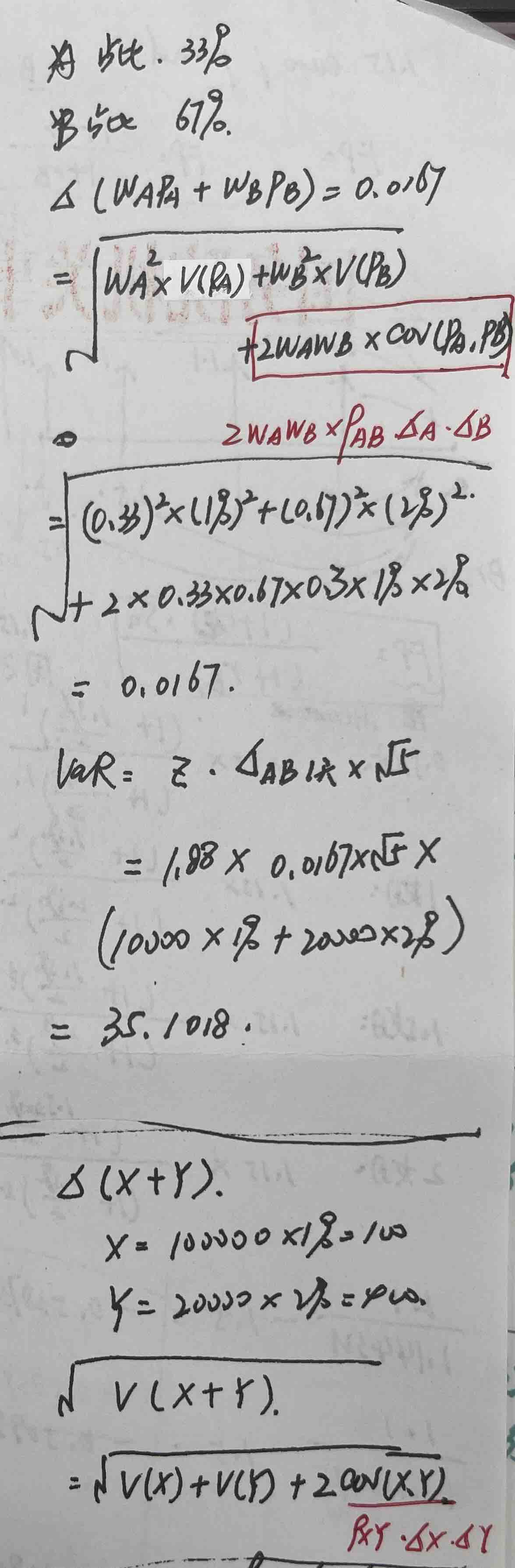

Consider a position consisting of a USD 10,000 investment in asset X and a USD 20,000 investment in asset Y. Assume that the daily volatilities of X and Y are 1% and 2% and that the coefficient of correlation between their returns is 0.3. What is the five-day VaR with a 97% confidence level?

解释:

The standard deviation of the daily changes in the assets are (in USD) 100 and 400. The standard deviation of the daily change in the portfolio is (100^2+400^2+2×100×400×0.3)^0.5=440.5

The standard deviation of the five-day change is the square root of 5 multiplied by the one-day standard deviation, which is USD 984.9. The 97% VaR is 1.88 times this, which is USD 1852.4.

题目问:有一个头寸包含10,000$的资产X,20,000$的资产Y,假设每日波动是1%和2%,相关系数是0.3,求5天97%的VaR?

每日波动的dollar值:X=10,000*1%=100,Y=20,000*2%=400

组合每日的波动=(100^2+400^2+2×100×400×0.3)^0.5=440.5

5天97%的VAR=440.5*(5)^0.5*1.88=1852.4

老师好,1、黑线上半部分我哪里想的不对吗?2、答案的解析,也就是黑线下半部分,我不明白为什么V(X+Y)就直接用100和400来算了,我明白100和400是怎么来的哈,但是100和400只是资产价值啊,100^2难道就相当于V(X)?400^2相当于V(Y)?cov(X,Y)相当于0.3*100*400?不懂答案的含义是什么意思,100就是西格玛X?400就是西格玛Y?3、如果用excel计算的话,有概率计算分位点是什么函数?有分位点计算累计概率又是什么函数呢