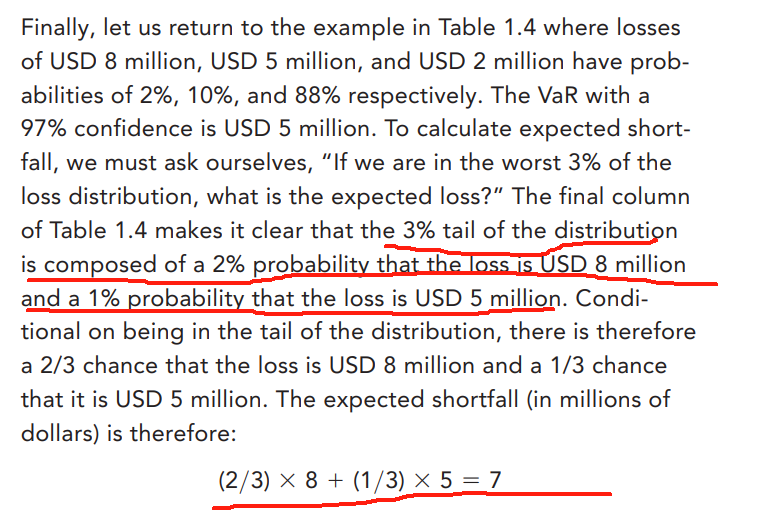

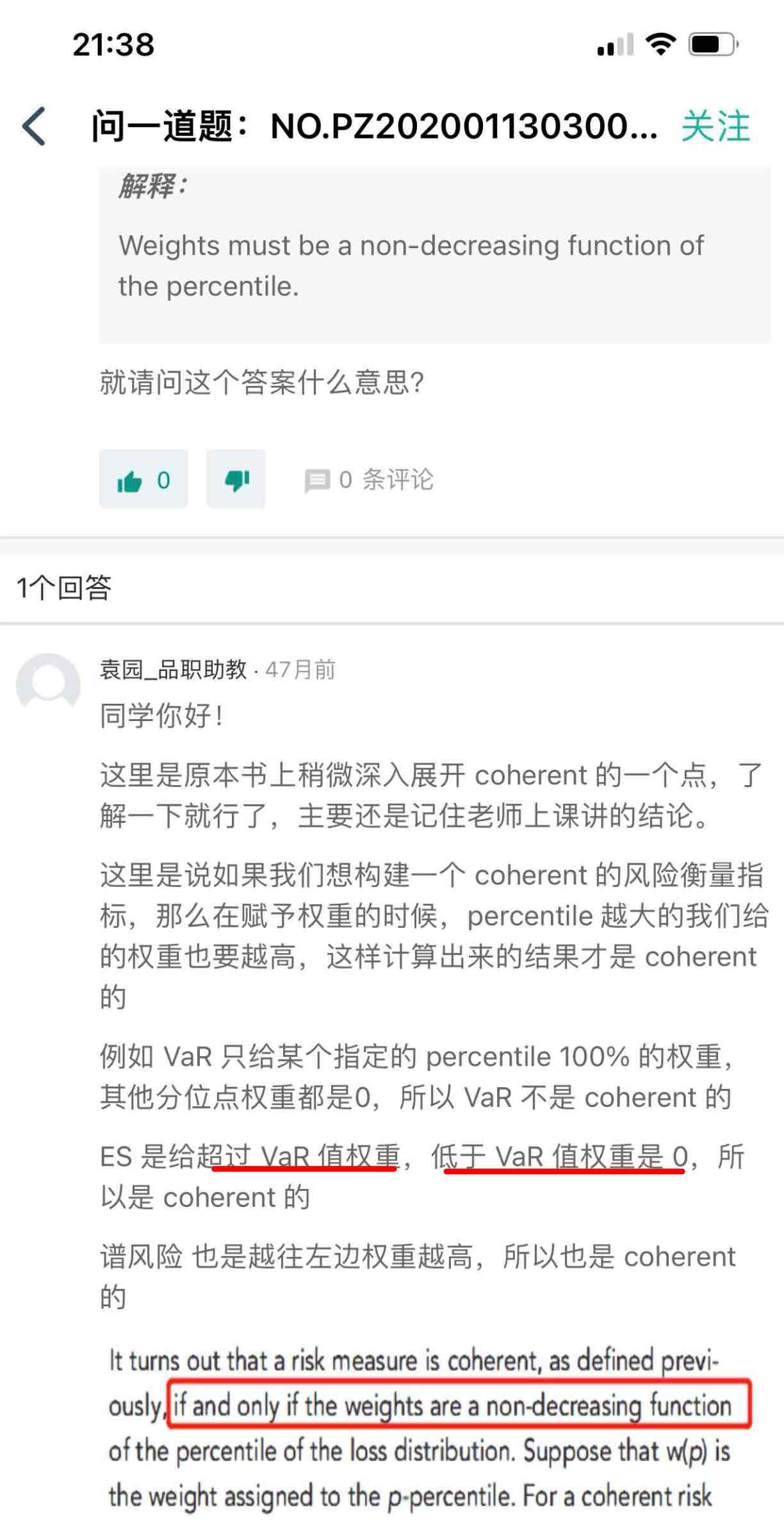

NO.PZ2020011303000046

问题如下:

When a risk measure is defined by assigning weights to percentiles, under what circumstances is it coherent?

解释:

Weights must be a non-decreasing function of the percentile.

当通过为百分位数分配权重来定义风险度量时,在什么情况下它是一致的?

权重必须是百分位数的非递减函数。

老师好,ES不是应该给大于等于VaR的损失权重吗?就是也包括VaR那个分位点