NO.PZ2023090401000071

问题如下:

Question A risk manager at a bank is measuring the sensitivity of a bond portfolio to non-parallel shifts in spot rates. The portfolio currently holds a 4-year zero coupon bond and a 7-year zero coupon bond with the following sensitivities to these respective spot rates:

To model the non-parallel movement of the spot rate curve, the manager treats the 2-year, 5-year, and 10-year spot rates as key rates. Given this information, what is the portfolio’s key rate 01 (KR01) for a 1-bp increase in the 5-year rate?

选项:

A.

AUD 184.06

B.

AUD 226.99

C.

AUD 307.66

D.

AUD 491.72

解释:

Explanation:

C is correct. For a key rate (or partial) 01, the magnitude of a shift in a key rate declines linearly to zero at the next key rate above and/or below. Therefore, if the 5- year spot rate increases by 1 bp, the 4-year and 7-year spot rates change as follows:

4-year spot rate:

1 ∗ (4 – 2) / (5 – 2) = 0.6667

7-year spot rate:

1 ∗ (10 – 7) / (10 – 5) = 0.6

The change in the value of the portfolio for a 1 bp change in the 5-year spot rate is therefore:

0.6667 ∗ −189.27 + 0.6 ∗ −302.45 = 307.6563

A is incorrect. This incorrectly calculates the changes in the 4-year and 7-year rates as 0.3333 and 0.4 respectively.

B is incorrect. This incorrectly calculates the change in the 7-year rate as 0.3333.

D is incorrect. This incorrectly calculates the forward bucket 01 for the portfolio, assuming the 4-year and 7-year rates change by 1.

Section: Valuation and Risk Models

Learning Objective: Define, calculate, and interpret key rate 01 and key rate duration.

Reference: Global Association of Risk Professionals. Valuation and Risk Models. New York, NY: Pearson, 2022. Chapter 13. Modeling Non-Parallel Term Structure Shifts and Hedging.

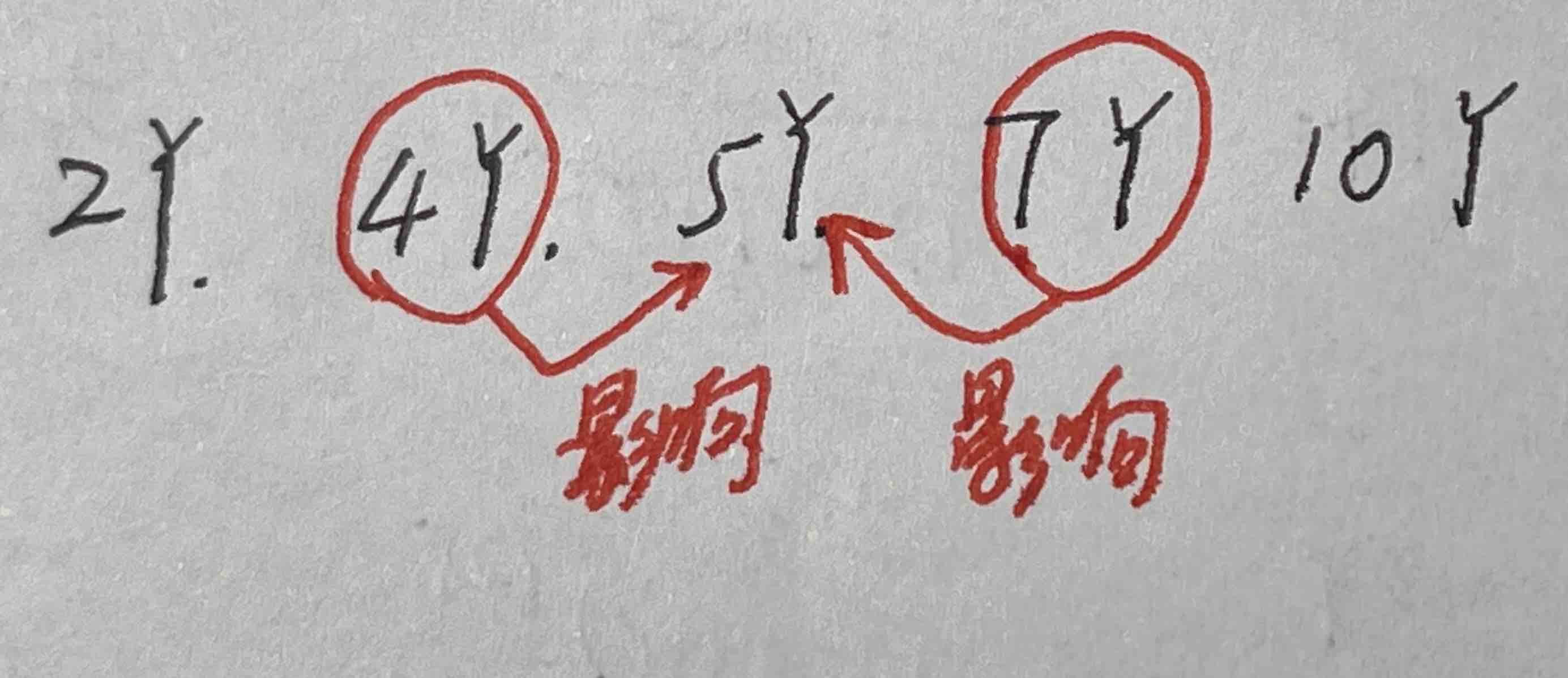

老师好,这道题

我不明白,为什么4Y spot rate对5Y spot rate的影响不是“(5-4)/(5-2)?7Y spot rate对5Y spot rate的影像不是“(7-5)/(10-5)”?