NO.PZ2020011303000214

问题如下:

Does convexity increase or decrease the profit from a small parallel shift in rates for a long position in a bond?

解释:

题目问:对于long position,在利率出现小幅平行移动时,凸性会增加还是减少债券的收益?

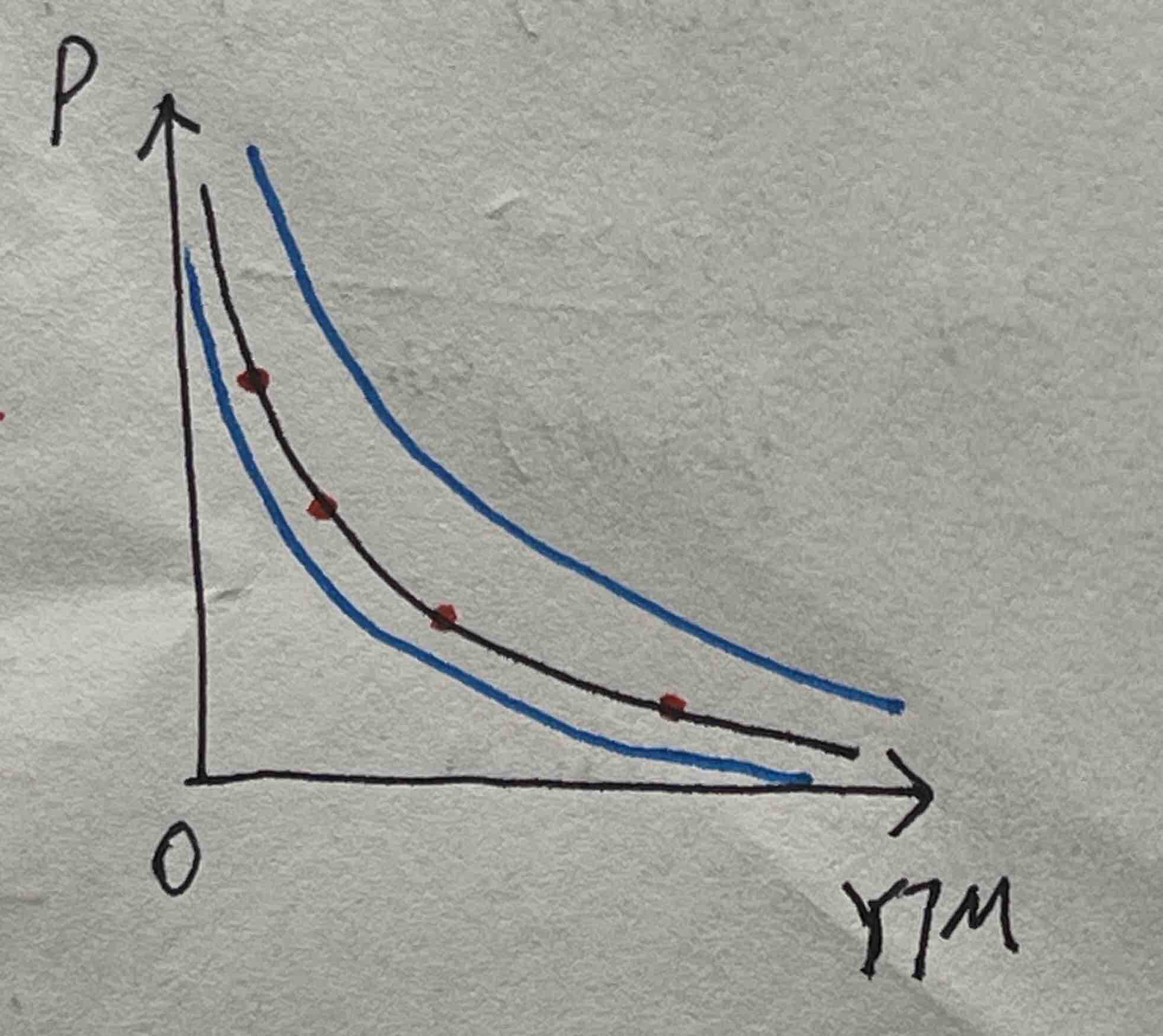

It increases the profit. 会增加收益,因为债券价格涨多跌少。

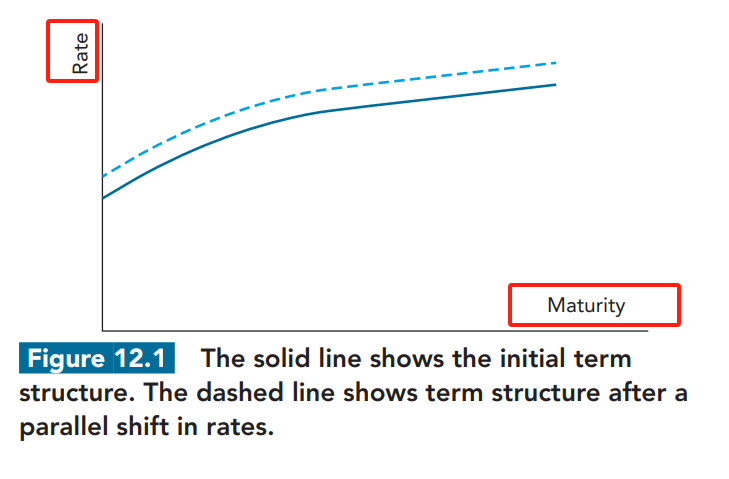

老师好,所谓利率平行移动是红色点的移动,还是蓝色的移动?还是什么?能否画个图举个例子?