NO.PZ2023020101000016

问题如下:

Mehta, who is based in Hong Kong SAR and

requires a €25,000,000 one-year bridge loan to fund operations in Germany. He

wants to fund this loan at a competitive rate. Riley advises Mehta to borrow in

HK dollars and enter into a one-year foreign currency swap to swap into euros.

The current exchange rate is HK$9.15 per euro. Exhibit 1 below provides Hong

Kong and euro spot interest rates and present value factors.

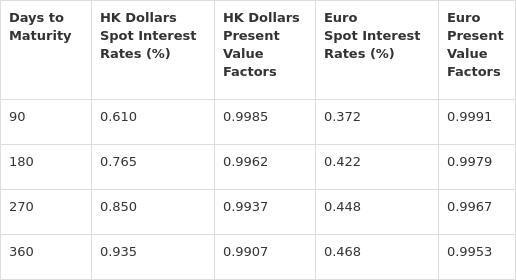

Exhibit

1: Hong Kong and Euro Spot Interest Rates

Based on the information in Exhibit 1, the

annual fixed swap rate Mehta would pay is closest

to:

选项:

A.0.47%.

0.92%.

C.

1.88%.

解释:

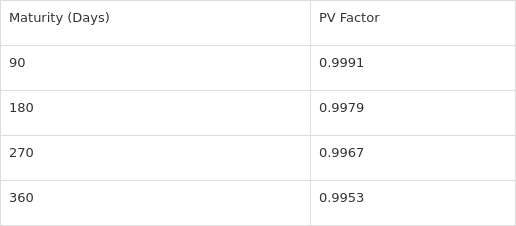

PV

factors for Euro are provided along with an explanation of how they are

calculated:

For

example, PV(90) is calculated as follows:

Other

present value factors are calculated in a similar manner.

The

fixed rate is calculated as follows:

The

annualized rate = 0.001178 × 4 = 0.004712.

老师,你好,我是这样做的,不知道为什么不对:

事件发生:

T0: borrow 25mn *9.15 HKD for EURO25mn;

T1: return HKD: 25*9.15 *(1+0.0935%).

Cash flow:

1.我没有假设quarterly compounding,认为t=1是唯一现金流交换时间

2.因为通过swap得到欧元,所以支付欧元;被支付港币floating rate

at t1:

c = 25mn EURO * swap rate

float leg = 25mn * 9.15 * 0.935%

在t1时候,EUR/HKD Swap back。

那么c & float leg discount to t0应该价格相等:

25mn EURO * swap rate *0.9953 = 25mn * 9.15 * 0.935% * 0.9907

所以swap rate = 8.5%.....

请问问题是哪里,而且为什么是quarterly compounding?