NO.PZ2020021204000052

问题如下:

Consider a currency swap where interest on British pounds at the rate of 3% is paid and interest on euros at 2% is received. The British pound principal is 1.0 million pounds and the euro principal is 1.1 million euros. The most recent exchange has just occurred and the interest is exchanged every six months. There are two years are remaining in the life of the swap. The current exchange rate is 1.15 euro/pound. The risk-free rates in pounds and euros are 2.5% and 1.5%. Value the swap by considering it as the difference between two bonds. All rates are compounded semi-annually.

Value the swap above by considering it as a portfolio of forward contracts.

解释:

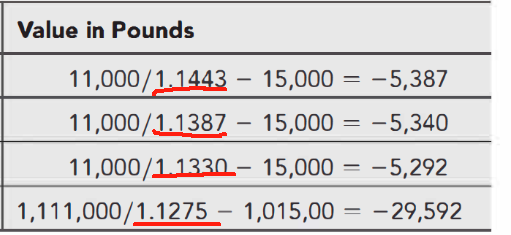

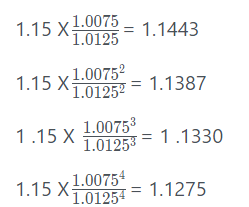

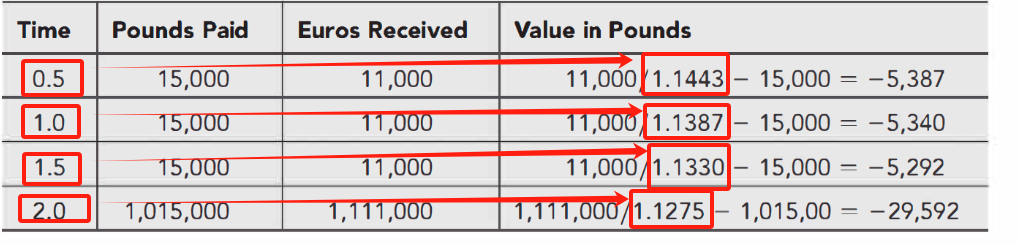

The forward rates corresponding to the exchanges at times 0.5, 1.0, 1.5, and 2.0 years are

1.15 X= 1.1443

1.15 X= 1.1387

1 .15 X = 1 .1330

1.15 X= 1.1275

The exchanges are

The GBP value of the swap is

----= -43,785

老师好,能帮了看看我哪里计算错了吗?