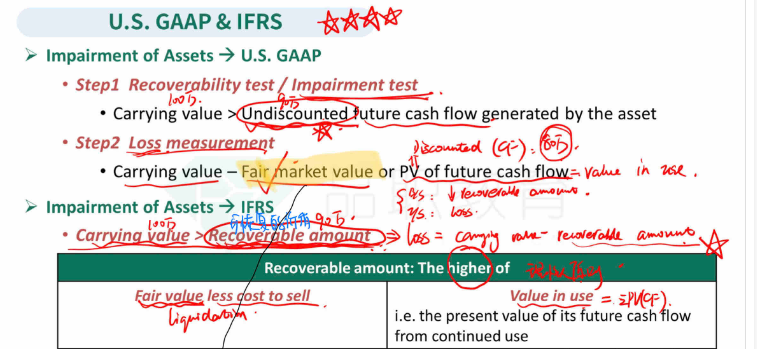

如题,假设此题undiscounted expected future cash flows为49000,那么在美国准则下,

- 应该用fair market value还是pv of future cash flow呢?

- fair market value是55000,还是46000呢,即是否要减costs to sell?

14:08 (2X)

lynn_品职助教 · 2024年07月12日

嗨,努力学习的PZer你好:

需要调整这个资产的Fair value (没有fair value 再调整到pv of future cash flow)

2.fair market value是55000,还是46000呢,即是否要减costs to sell?

不减。

IFRS:

减值测试:The entire carrying amount of investment > recoverable amount with its carrying amount

减值损失:The impairment loss is recognized on the IS.

US GAAP:

减值测试:if The fair value of the investment declines below its carrying value and the decline is determined to be permanent.

减值损失:Impairment loss to be recognized on IS, and the carrying value of the investment on BS is reduced to its fair value.

所以对于GAAP,impairment loss=carrying value -fair value=49500-55000=(实际上不用减值,因为减值测试就不用)

而对于IFRS,impairment loss=carrying value-recoverable amount

recoverable amount=max(net selling price,value in use).即net selling price 和value in use取高

net selling price=fair value-costs to sell。

value in use 是未来现金流的现值。

----------------------------------------------虽然现在很辛苦,但努力过的感觉真的很好,加油!