NO.PZ2023052301000051

问题如下:

A bond pays a semiannual fixed coupon of 4.70%. It trades at par on its coupon date of 16 December 2025 and matures on 16 December 2033. The bond’s annualized convexity statistic is closest to:

选项:

A.51.670

53.231

206.681

解释:

A is correct.

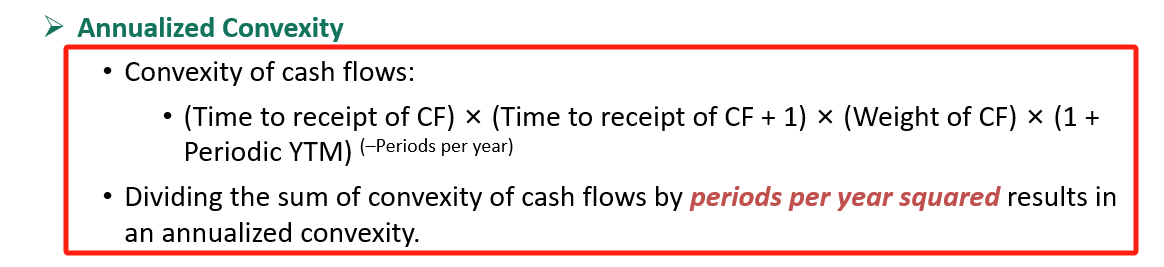

t*(t+1)*W/(1+Yn)的n次方,Yn是一期的利率,n是一年计息次数。对吗?n并不是都等于2