NO.PZ2020021205000024

问题如下:

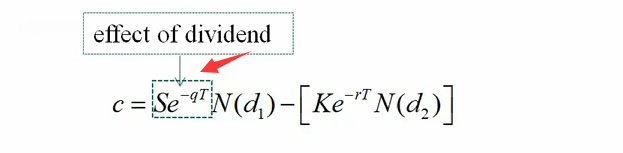

How is the Black-Scholes-Merton formula used to value European options on a dividend-paying stock?

解释:

The present value of the dividends that have ex-dividend dates during the life of the option is subtracted from the stock price when the formula is used. The volatility applies to the stock price minus the present value of the dividends. In this context, a dividend is defined as the reduction in the stock price on the ex-dividend date.

在BSM这张的波动率章节不是提到,分红和税并没有真的使股票价格下跌,所以不考虑分红和税就可以了,波动率不变。但是红色线好想说的是波动率应用于股价减去分红的现值,是想说啥?