NO.PZ2020021205000064

问题如下:

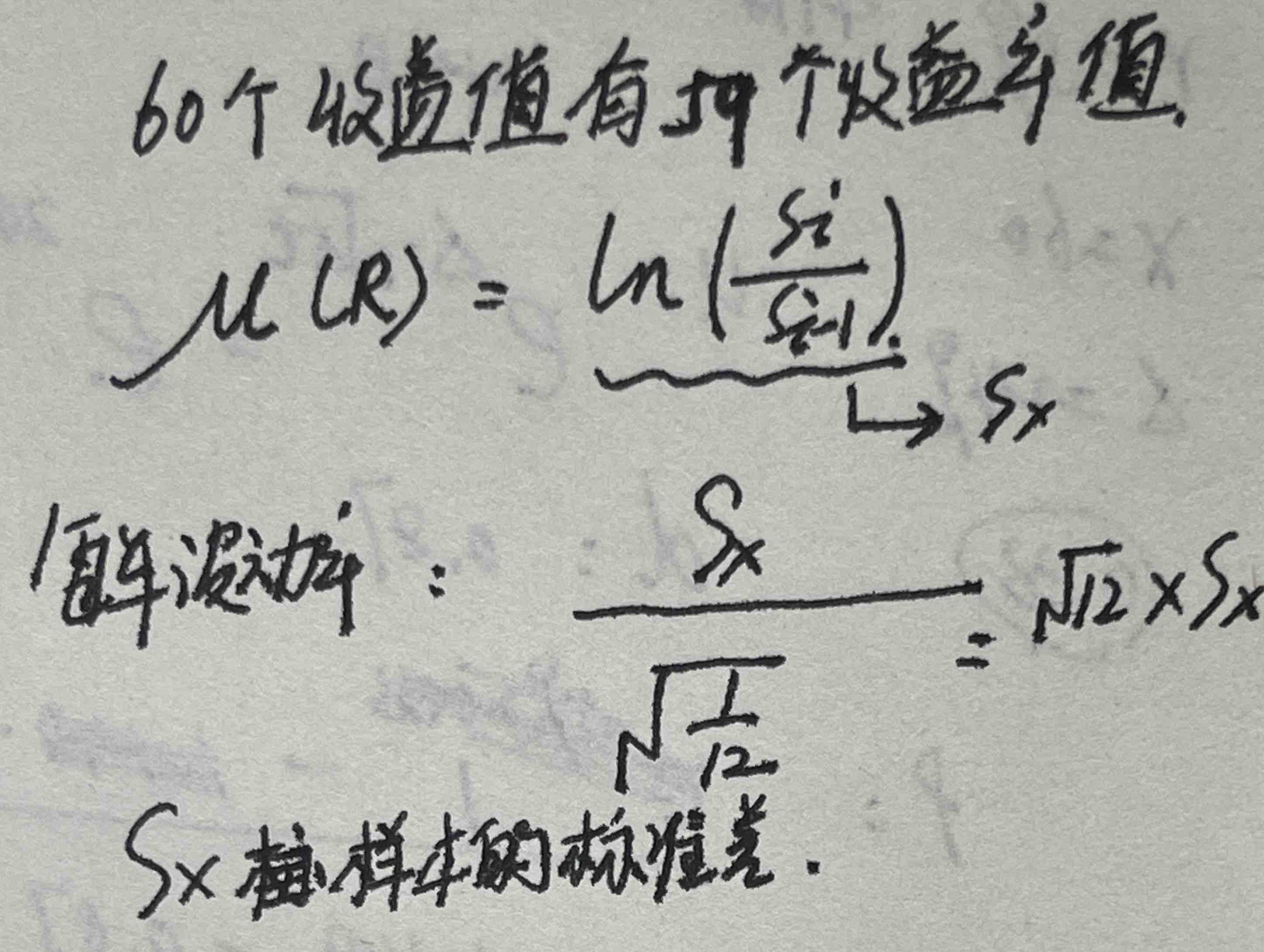

If you have five years of monthly data on a variable, how would you calculate its volatility?

解释:

If is the value of the variable at the end of month i, the volatility is times the standard deviation of the 59 values of

老师好,我写的这个过程有不对的地方吗?