NO.PZ201809170400000603

问题如下:

Ayanna Chen is a portfolio manager at Aycrig Fund, where she supervises assistant portfolio manager Mordechai Garcia. Aycrig Fund invests money for high-net-worth and institutional investors. Chen asks Garcia to analyze certain information relating to Aycrig Fund’s three submanagers, Managers A, B, and C.

Manager A has $250 million in assets under management (AUM), an active risk of 5%, an information coefficient of 0.15, and a transfer coefficient of 0.40. Manager A’s portfolio has a 2.5% expected active return this year.

Chen directs Garcia to determine the maximum position size that Manager A can hold in shares of Pasliant Corporation, which has a market capitalization of $3.0 billion, an index weight of 0.20%, and an average daily trading volume (ADV) of 1% of its market capitalization.

Manager A has the following position size policy constraints:

Allocation: No investment in any security may represent more than 3% of total AUM.

Liquidity: No position size may represent more than 10% of the dollar value of the security’s ADV.

Index weight: The maximum position weight must be less than or equal to 10 times the security’s weight in the index.

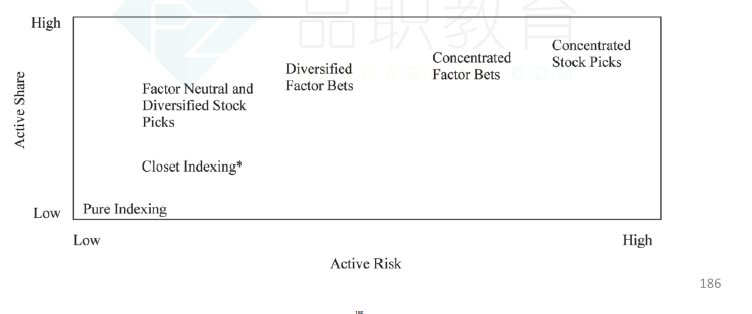

Manager B holds a highly diversified portfolio that has balanced exposures to rewarded risk factors, high active share, and a relatively low active risk target.

Selected data on Manager C’s portfolio, which contains three assets, is presented in Exhibit 1.

Chen considers adding a fourth sub-manager and evaluates three managers’ portfolios, Portfolios X, Y, and Z. The managers for Portfolios X, Y, and Z all have similar costs, fees, and alpha skills, and their factor exposures align with both Aycrig’s and investors’ expectations and constraints. The portfolio factor exposures, risk contributions, and risk characteristics are presented in Exhibits 2 and 3.

Chen and Garcia next discuss characteristics of long–short and long-only investing. Garcia makes the following statements about investing with long–short and long-only managers:

Statement 1 A long–short portfolio allows for a gross exposure of 100%.

Statement 2 A long-only portfolio generally allows for greater investment capacity than other approaches, particularly when using strategies that focus on large-cap stocks.

Chen and Garcia then turn their attention to portfolio management approaches.Chen prefers an approach that emphasizes security-specific factors, engages in factor timing, and typically leads to portfolios that are generally more concentrated than those built using a systematic approach.

Manager B’s portfolio is most likely consistent with the characteristics of a:

选项:

A.pure indexer.

B.sector rotator.

C.multi-factor manager.

解释:

C is correct. Most multi-factor products are diversified across factors and securities and typically have high active share but have reasonably low active risk (tracking error), often in the range of 3%. Most multi-factor products have a low concentration among securities in order to achieve a balanced exposure to risk factors and minimize idiosyncratic risks. Manager B holds a highly diversified portfolio that has balanced exposures to rewarded risk factors, a high active share, and a relatively low target active risk—consistent with the characteristics of a multi-factor manager.

书本上权重策略说了6种,是否可以按照已下归类

- Active risk 和Active share 都高:concentrated stock picks & concentrated factor(也叫sector rotator)

- Active risk 低,active share 高:diversified factor(也叫multiple factor) & netural factor and diversifed stock picks

- Acitve riks 低,active share 低: closet indexing & pure indexing

另外,每一种策略是否有别名啊?

、

、