NO.PZ2023040601000019

问题如下:

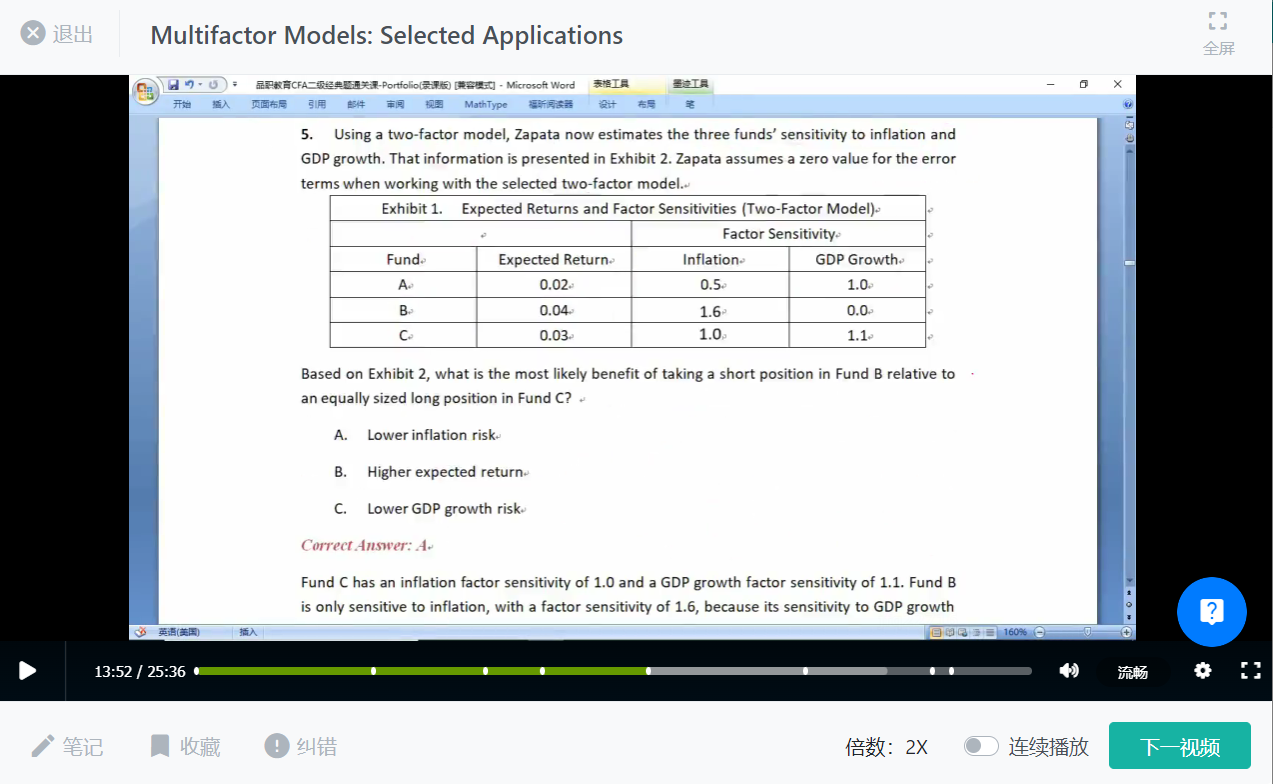

Using a two-factor model, Zapata now estimates the three funds’ sensitivity to inflation and GDP growth. That information is presented in Exhibit 2. Zapata assumes a zero value for the error terms when working with the selected two-factor model.

Based on Exhibit 2, what is the most likely benefit of taking a short position in Fund B relative to an equally sized long position in Fund C?

选项:

A.Lower inflation risk

Higher expected return

Lower GDP growth risk

解释:

Fund C has an inflation factor sensitivity of 1.0 and a GDP growth factor sensitivity of 1.1. Fund B is only sensitive to inflation, with a factor sensitivity of 1.6, because its sensitivity to GDP growth is zero. Relative to an investment in Fund C, a short position in Fund B would reduce exposure to inflation risk, and it would have no impact on the existing GDP growth risk exposure. It is unclear whether the expected return would increase or decrease.

这道题不理解,麻烦解析一下