NO.PZ201809170300000107

问题如下:

Yandie Izzo manages a dividend growth strategy for a large asset management firm. Izzo meets with her investment team to discuss potential investments in three companies: Company A, Company B, and Company C. Statements of cash flow for the three companies are presented in Exhibit 1.

Exhibit 1. Statements of Cash Flow, Most Recent Fiscal Year End (Amounts in Millions of Dollars)

Izzo’s team first discusses key characteristics of Company A. The company has a history of paying modest dividends relative to FCFE, has a stable capital structure, and is owned by a controlling investor.

The team also considers the impact of Company A’s three non-cash transactions in the most recent year on its FCFE, including the following:

Transaction 1: A $900 million loss on a sale of equipment

Transaction 2: An impairment of intangibles of $400 million

Transaction 3: A $300 million reversal of a previously recorded restructuring charge

In addition, Company A’s annual report indicates that the firm expects to incur additional non-cash charges related to restructuring over the next few years.

To value the three companies’ shares, one team member suggests valuing the companies’ shares using net income as a proxy for FCFE. Another team member proposes forecasting FCFE using a sales-based methodology based on the following equation:

FCFE = NI- (1 - DR)(FCInv - Dep) - (1 - DR)(WCInv)

Izzo’s team ultimately decides to use actual free cash flow to value the three companies’ shares. Selected data and assumptions are provided in Exhibit 2.

Exhibit 2. Supplemental Data and Valuation Assumptions

The team calculates the intrinsic value of Company B using a two-stage FCFE model. FCFE growth rates for the first four years are estimated at 10%, 9%, 8%, and 7%, respectively, before declining to a constant 6% starting in the fifth year.

To calculate the intrinsic value of Company C’s equity, the team uses the FCFF approach assuming a single-stage model where FCFF is expected to grow at 5% indefinitely.

Based on Exhibits 1 and 2 and the proposed single-stage FCFF model, the intrinsic value of Company C’s equity is closest to:

选项:

A.$277,907 million.

B.$295,876 million.

C.$306,595 million.

解释:

C is correct. Company C’s firm value is calculated as follows:

The required rate of return on equity for Company C is

r = E(Ri) = RF + βi[E(RM) RF] = 3% + 1.1(7%) = 10.7%.

WACC = rd (1 - Tax rate) + re

WACC = 0.40(6%)(1 0.30) + 0.60(10.7%) = 1.68% + 6.42% = 8.10%

FCFF for the most recent year for Company C is calculated as follows:

Investment in working capital is found by adding the increase in accounts receivable, the increase in inventories, the decrease in accounts payable, and the increase in other current liabilities: $536 million $803 million $3 million + $350 million = $992 million.

FCFF is expected to grow at 5.0% indefinitely. Thus,

Firm

value =  =

=  =

=  = $510,990.97 million

= $510,990.97 million

The value of equity is the value of the firm minus the value of debt. The value of debt is found by multiplying the target debt ratio by the total firm value:

Debt value = 0.40($510,990.97) = $204,396.39

Therefore, equity value = $510,990.97 $204,396.39 = $306,594.58 million.

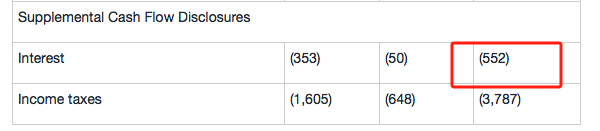

CFO中的数据,是真金白银的流出/入,所以我做的时候想的就是552就是真正税后的利息费用,虽然不影响选答案吧,但还是想了解下原因