NO.PZ202207040100000605

问题如下:

The portfolio method suggested by Stapleton to replicate the MSCI EAFE Index is best described as:

选项:

A.optimization.

B.stratified sampling.

C.a blended approach.

解释:

SolutionB is correct. The portfolio method that Stapleton is describing is stratified sampling. In equity indexing, stratified sampling methods are most frequently used when the portfolio manager wants to track indexes that have a large number of constituents or when dealing with a relatively low level of assets under management. In stratified sampling, the portfolio manager holds a limited sample of the index constituents arranged in distinct strata or subgroupings. Arranged correctly, the various strata will be mutually exclusive and also exhaustive and should closely match the characteristics and performance of the index.

A is incorrect. Optimization typically involves maximizing a desirable characteristic or minimizing an undesirable characteristic, subject to one or more constraints.

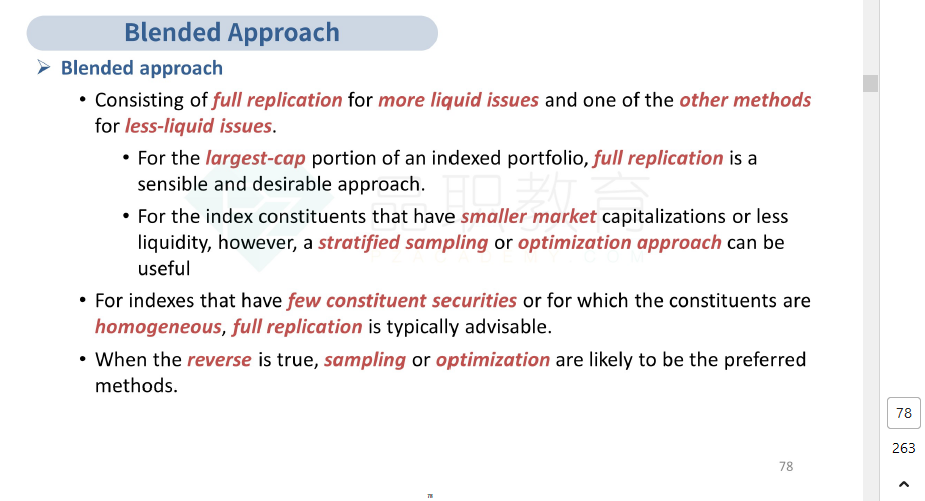

C is incorrect. An indexed portfolio can be managed using a blended approach consisting of full replication for more liquid issues and stratified sampling or optimization for less liquid issues.

根据解答,说的是blended approach适合资产量大的情况,希望再解答一下什么情况下以及什么条件适用这个方法