请问 -1.4从何而来?

问题如下图:

选项:

A.

B.

C.

解释:

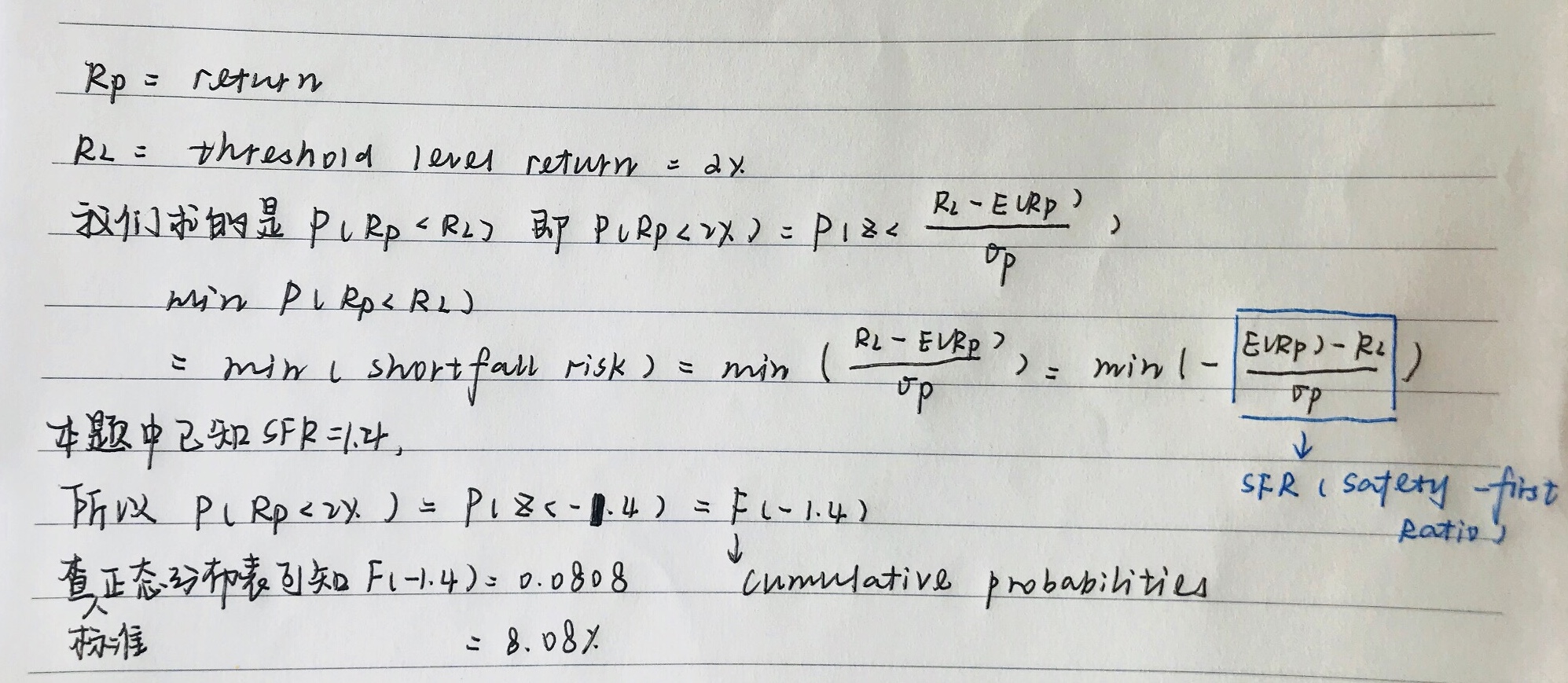

NO.PZ2015120604000108 问题如下 If a Portfolio's SFR is 1.4 an threshollevel's return is supposeto 2%, whis the probability of return less th2%?[F(1.4)=0.9192] A.8.08%. B.30.20%. C.9.68%. A is correct.Using the table, we get F( -1.4) is 1 - 0.9192 = 8.08%. 考试里会有需要查表的题目吗?考试里会有需要查表的题目吗?

NO.PZ2015120604000108问题如下 If a Portfolio's SFR is 1.4 an threshollevel's return is supposeto 2%, whis the probability of return less th2%?[F(1.4)=0.9192] A.8.08%.B.30.20%.C.9.68%.A is correct.Using the table, we get F( -1.4) is 1 - 0.9192 = 8.08%.本题解题思路是什么,为什么涉及分布问题

NO.PZ2015120604000108 问题如下 If a Portfolio's SFR is 1.4 an threshollevel's return is supposeto 2%, whis the probability of return less th2%?[F(1.4)=0.9192] A.8.08%. B.30.20%. C.9.68%. A is correct.Using the table, we get F( -1.4) is 1 - 0.9192 = 8.08%. 为啥要标准化,已经F1.4的意义,这块忘记了。补补吧,课程里有吗

NO.PZ2015120604000108问题如下 If a Portfolio's SFR is 1.4 an threshollevel's return is supposeto 2%, whis the probability of return less th2%?[F(1.4)=0.9192] A.8.08%.B.30.20%.C.9.68%.A is correct.Using the table, we get F( -1.4) is 1 - 0.9192 = 8.08%.这题是否一定需要查表吗? 因為用1 減去題目0.9192 也是剛好0.0808,这种方法是巧合吗?

NO.PZ2015120604000108 问题如下 If a Portfolio's SFR is 1.4 an threshollevel's return is supposeto 2%, whis the probability of return less th2%?[F(1.4)=0.9192] A.8.08%. B.30.20%. C.9.68%. A is correct.Using the table, we get F( -1.4) is 1 - 0.9192 = 8.08%. SFR的全称是什么呢,不记得了