NO.PZ2024042601000048

问题如下:

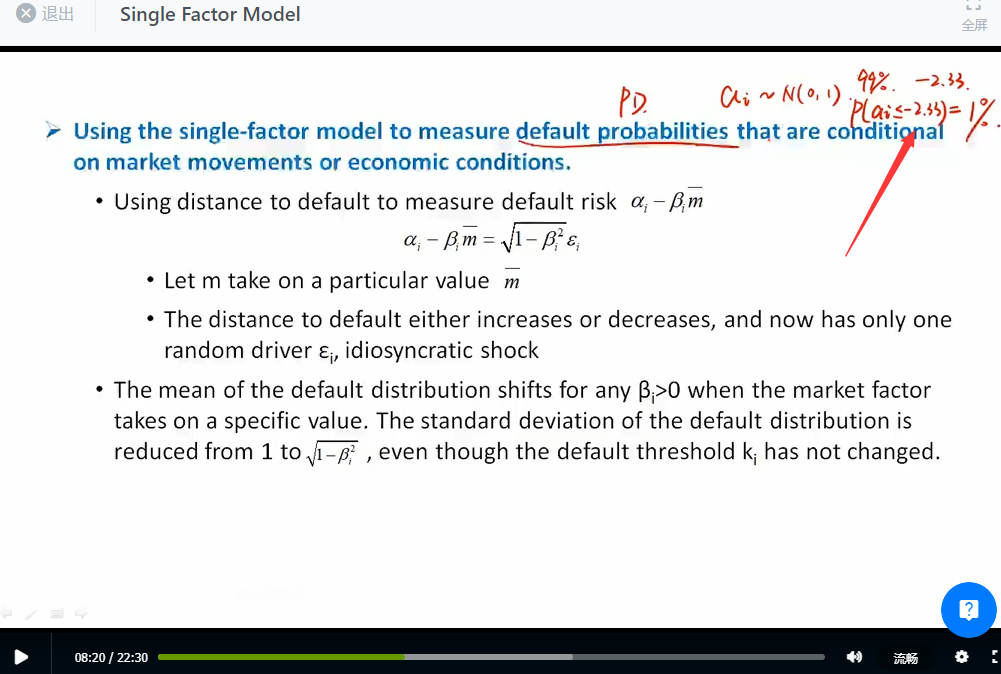

Under single-factor model, a firm has a beta of 0.40 and an unconditional default probability of 1%. If we enter a modest economic downturn, such that the value of m = -1.0, what is the conditional default probability?

选项:

A.1.0%

B.1.8%

C.2.5%

D.2.8%

解释:

结果是查表么