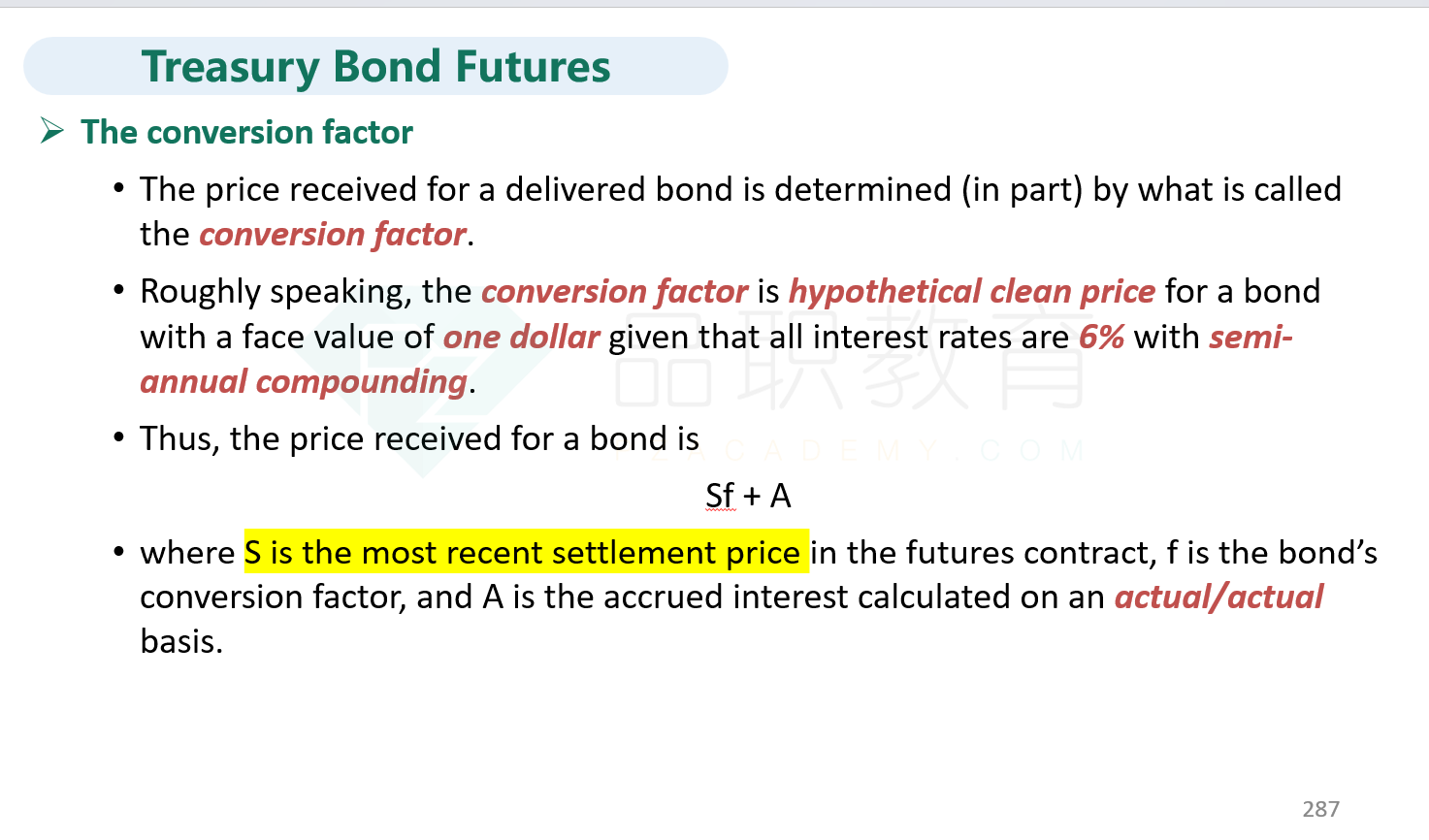

NO.PZ2019052801000044

问题如下:

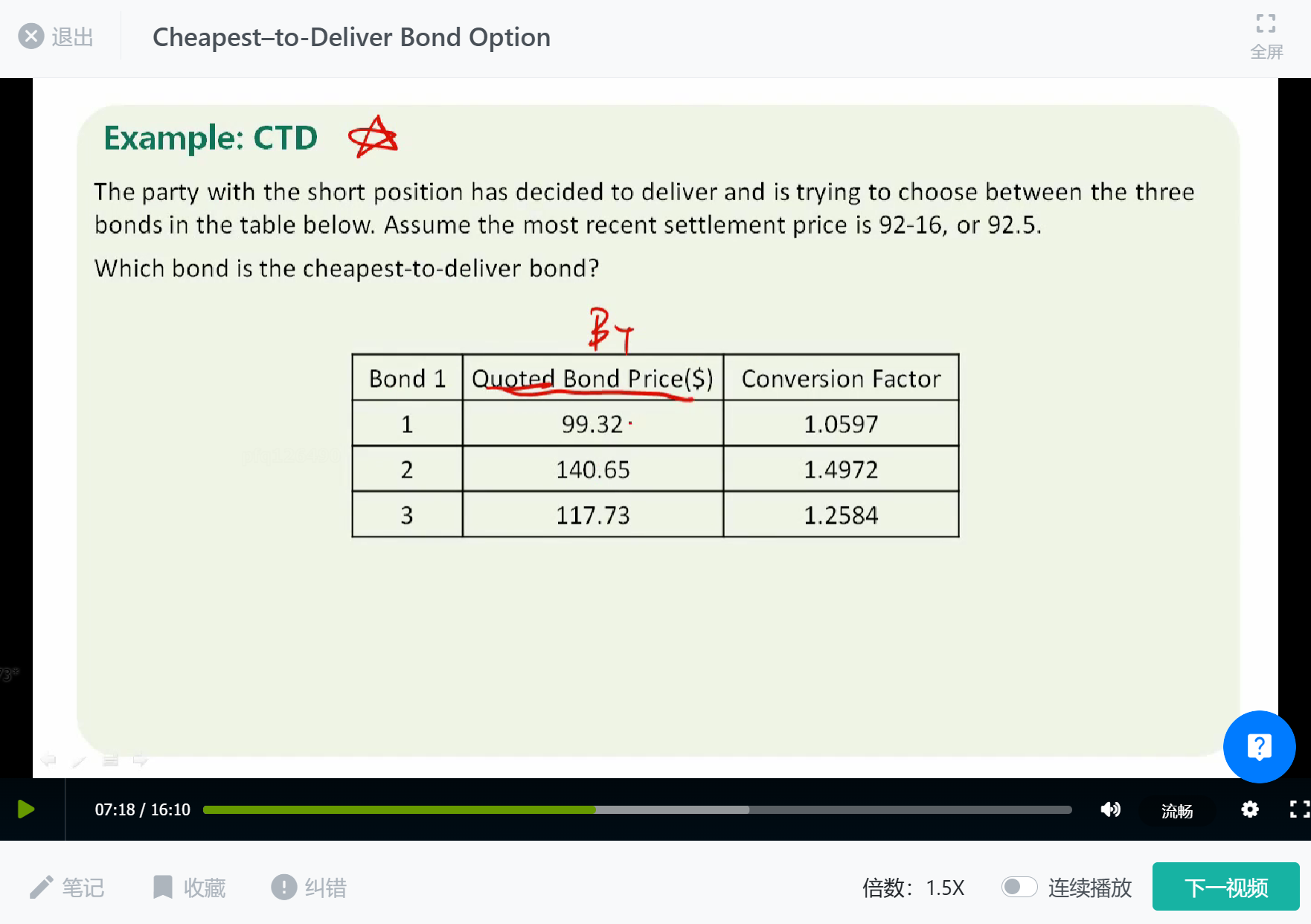

The party with the short position has decided to deliver and is trying to choose between the three bonds in the table below. Assume the most recent settlement price is 92-16, or 92.5. Which bond is the cheapest-to-deliver bond?

选项:

A.

Bond 1.

B.

Bond 2.

C.

Bond 3.

D.

Bond 4.

解释:

A is correct.

考点:Interest Rate Derivative-Interest rate Futures

解析:

Bond 1: 99.32-(92.5×1.0597)=$1.2978

Bond 2: 140.65-(92.5×1.4972)=$2.1590

Bond 3: 117.73-(92.5×1.2584)=$1.3280

Bond 4: 129.54-(92.5×1.3762)=$2.2415

Bond 1最小,所以cheapest-to-deliver bond是Bond 1。

老师好,有两个问题:

1、按照课程的公式:CTD=最便宜的债券

即等于 short方买债券的成本-收到的钱

课里给的公式是:BondT-QFP*CF

按照这个公式,BondT应该是交割价格92.5%,而期货报价QFP*CF是期货到期short收到的钱啊,

bond1的CTD应该是92.5%-QFP1*CF1,以此类推才对啊。我看也有别的同学问了和我相同的问题,但老师的解释没有让我明白,看了反而更糊涂了。

2、在推倒CTD时,有AIT

购买成本是BT+AIT(是T时刻lshort在市场买债券时支付卖方的AI吗?)

T交割日收到的钱是QFP*CF+AIT 这里为什么还要有一个AIT呢?short在市场买到债券再卖给long,应该是交割日当天操作完?哪里来的AIT要给short呢?