NO.PZ202206210100000504

问题如下:

In the candidates’ responses to Fox regarding the relevant characteristics of asset classes, the statement that is least accurate is:

选项:

A.Kelly’s regarding correlations. B.Trainor’s. C.Kelly’s regarding rebalancing.解释:

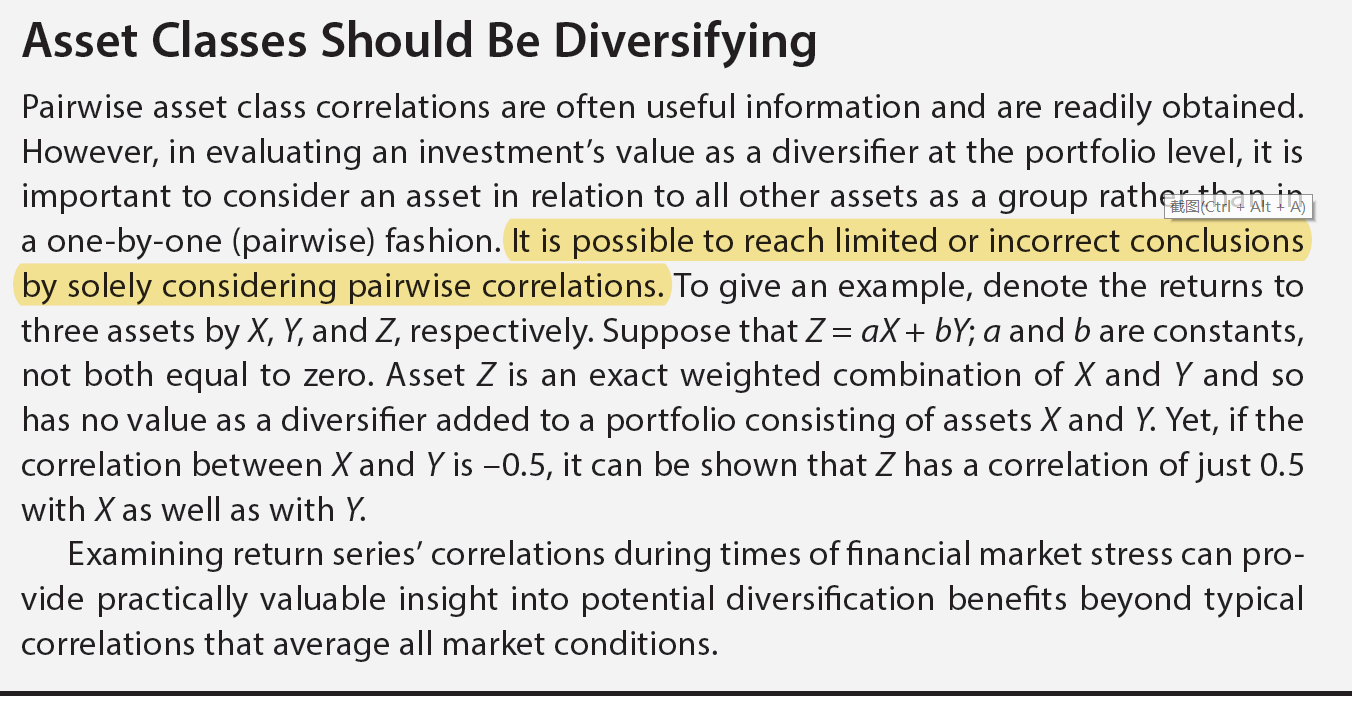

SolutioB is correct. Although Trainor is correct that asset classes should be diversifying, low pairwise correlations with other asset classes is not sufficient. An asset class may be highly correlated with some linear combination of the other asset classes even when pairwise correlations are not high. Both of Kelly’s comments are correct: Asset classes should have high within-group correlations but low correlations with other classes. If liquidity and transaction costs are unfavorable for an investment of a size meaningful for an investor, an asset class may not be a suitable investment for that investor.

B is correct. Although Trainor is correct that asset classes should be diversifying, low pairwise correlations with other asset classes is not sufficient. An asset class may be highly correlated with some linear combination of the other asset classes even when pairwise correlations are not high. Both of Kelly’s comments are correct: Asset classes should have high within-group correlations but low correlations with other classes. If liquidity and transaction costs are unfavorable for an investment of a size meaningful for an investor, an asset class may not be a suitable investment for that investor.

A is incorrect. Kelly’s first comment is correct about both the within-group and between class correlations.

C is incorrect. Kelly’s second comment is correct. The criteria that he is referring to is that asset classes should have the capacity to absorb a meaningful proportion of an investor’s portfolio. He is correct in saying that if liquidity and transaction costs are unfavorable for an investment of a size meaningful for an investor, an asset class may not be a suitable investment for the investor.

- Kelly: I like to stress to clients that asset classes should have high within-group correlations but low correlations with other classes. In addition, because investors need to rebalance to a strategic asset allocation, asset classes need to have both sufficient liquidity and low transaction costs.

- Trainor: It is important that asset classes should be diversifying. I always look for low pairwise correlations with other asset classes.

老师,题目中问的是least 准确性,也就找谁说的不对。

kelly说“asset classes need to have both sufficient liquidity and low transaction costs.”但是如果投资 real estate 这类资产的话,不可能要求高流动性和低成本啊,他的说法为什么是对的?

Trainor说“low pairwise correlations with other asset classes.”我看其他解答里,pairwise correlations是两两的相关性,也就是A与B、C要相关性低,且A与BC组合的相关性也要低,那他说的是low pairwise correlations,相关性低,这个说法为什么不对啊?