NO.PZ202312130100000303

问题如下:

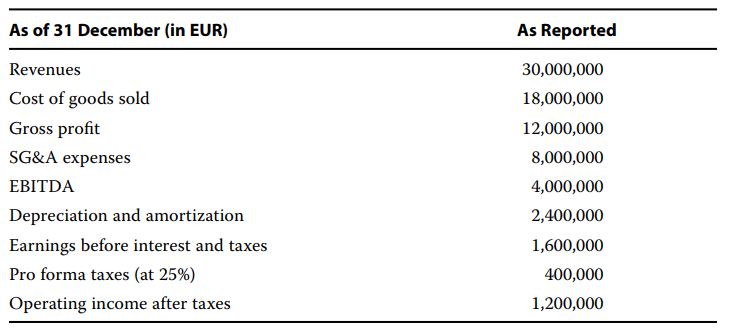

Schwalke is currently valuing LPE, a private furniture manufacturing company based in France. The company is owned entirely by the Lapiere family, with several family members employed as senior company managers. Jean Lapiere is the current CEO and owns 25% of LPE stock. LPE’s most recent income statement as part of its reviewed financial statements is as follows:

To estimate LPE’s required return on equity, Schwalke gathers betas from public furniture manufacturing companies, and after making appropriate adjustments, estimates LPE’s beta at 0.80. He uses an equity risk premium of 6%, a small-cap stock premium of 2%, a company-specific stock premium of 1.5%, and an industry risk premium of 1%.

After making other normalizing assumptions to LPE’s income statement and deducting the change in long-term assets of EUR 600,000 (equal to EUR 3,000,000 in capital expenditures less EUR 2,400,000 in depreciation), Schwalke estimates FCFF for the base year to be EUR 600,000. He decides to use the CCM in his income approach to valuing LPE with a WACC of 8% and perpetual growth of 4%.

Given the availability of similar publicly traded furniture manufacturing companies, Schwalke also uses a market approach to value LPE. He finds an average EV/ Sales multiple of 0.60 from these public comparable companies. Schwalke notes that LPE’s debt is currently EUR 6 million.

Jean Lapiere is seeking an estimate of the value of his LPE ownership stake. In the course of discussing the ownership structure, Schwalke concludes that none of the family members, including Jean, has a controlling interest in the company. Schwalke estimates discounts for lack of control and lack of marketability as 20% and 15%, respectively.

Which of the following is closest to the proper calculation of LPE’s EV using the CCM?

选项:

A.EUR 15 million

EUR 30 million

EUR 15.6 million

解释:

C is Correct. The CCM uses the following formula:

Recall that the FCFF at time t+1 must equal the base year FCFF multiplied by one plus the growth rate.

After making other normalizing assumptions to LPE’s income statement and deducting the change in long-term assets of EUR 600,000 (equal to EUR 3,000,000 in capital expenditures less EUR 2,400,000 in depreciation)

这里说了前面做了normalizing,把Asset减少了0.6M,那为什么最终计算的结果里面不把这个减掉呢?