NO.PZ2024021803000002

问题如下:

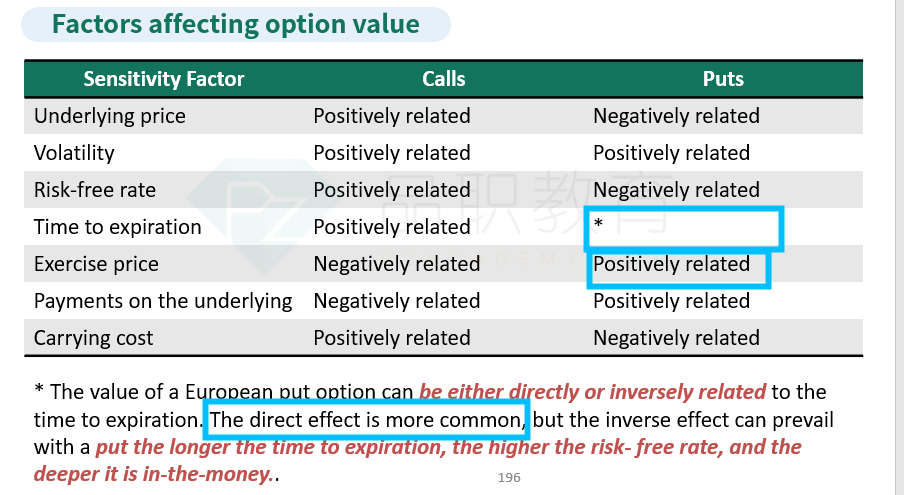

Considering all other factors as equal, which European put option listed below likely holds the greatest value?选项:

A.2 months, $52 B.4 months, $52 C.4 months, $58解释:

A European put option's value typically increases with both the length of time to expiration and the exercise price relative to the underlying price. Given the choices, the option with 4 months to expiration and a $58 exercise price would have the highest value. 欧式看跌期权的价值通常随着到期时间的延长和行权价格相对于标的价格的提高而增加。在给定的选项中,拥有4个月到期时间和58美元行权价格的期权将具有最高的价值。如题 , 是我 miss 了什么 还是我以后做题时需要assume 如果 没有specify 给出的价格那即为 exercise price?