NO.PZ2023091802000047

问题如下:

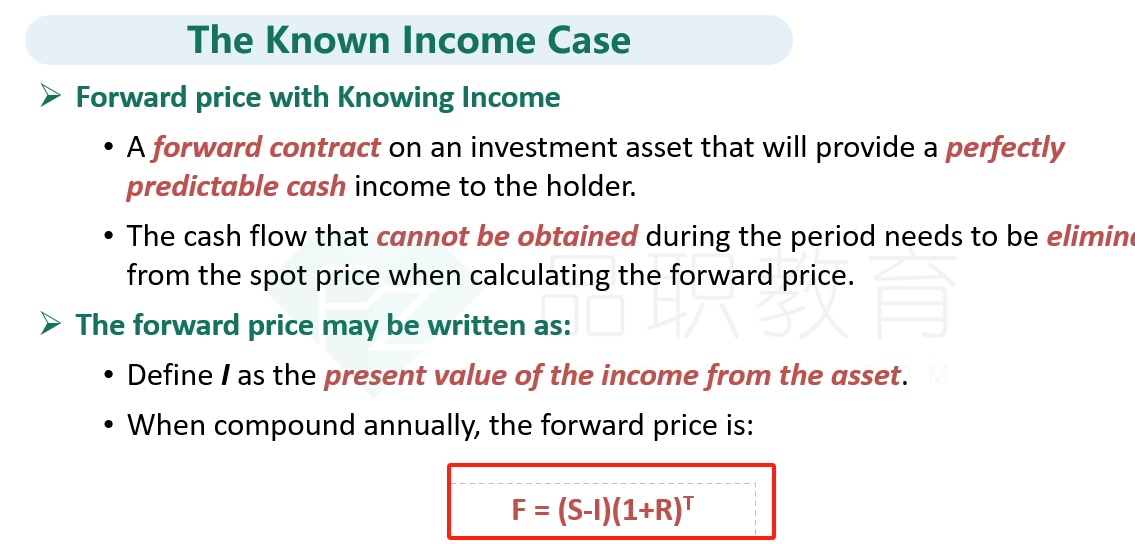

A risk analyst wants to enter into a 6-month forward contract on a USD 1,000 bond paying a 6% coupon semi-annually. A coupon is scheduled to be paid in three months. If the bond currently trades at par and the risk-free is 2%per year, the forward price should be closest to:

选项:

A.USD 960

B.USD 975

C.USD 980

D.USD 1,040

解释:

老师能再给我讲一下吗,没有太懂这个怎么求解