NO.PZ201712110200000405

问题如下:

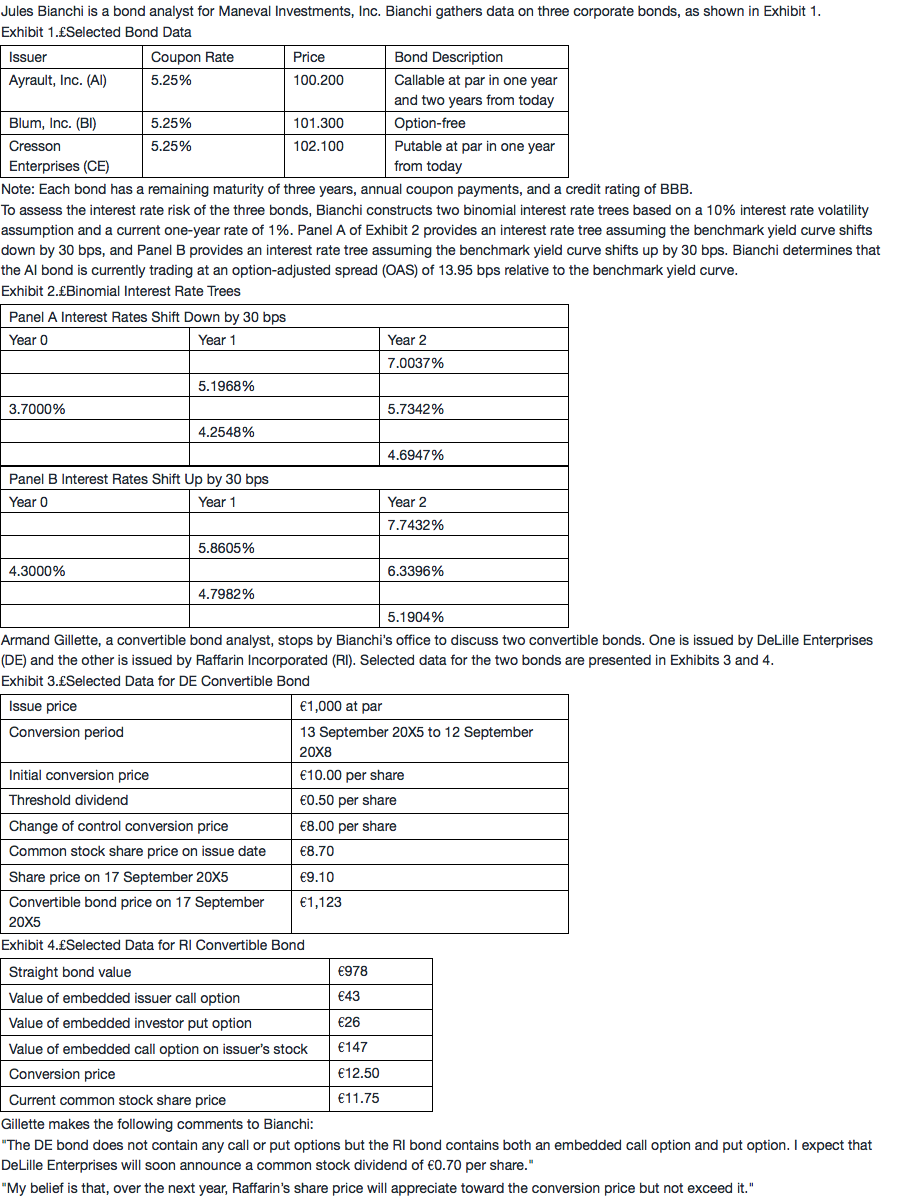

Which bond in Exhibit 1 most likely has the lowest effective convexity?

选项:

A.

AI bond

B.

BI bond

C.

CE bond

解释:

A is correct.

All else being equal, a callable bond will have lower effective convexity than an option-free bond when the call option is in the money. Similarly, when the call option is in the money, a callable bond will also have lower effective convexity than a putable bond if the put option is out of the money. Exhibit 1 shows that the callable AI bond is currently priced slightly higher than its call price of par value, which means the embedded call option is in the money. The put option embedded in the CE bond is not in the money; the bond is currently priced 2.1% above par value. Thus, at the current price, the putable CE bond is more likely to behave like the optionfree BI bond. Consequently, the effective convexity of the AI bond will likely be lower than the option-free BI bond and the putable CE bond.

请问还要判断ITM和OTM吗?是否可以统一记忆call option永远小于put option的ED因为call option负凸而put option more convex?