NO.PZ2023010903000072

问题如下:

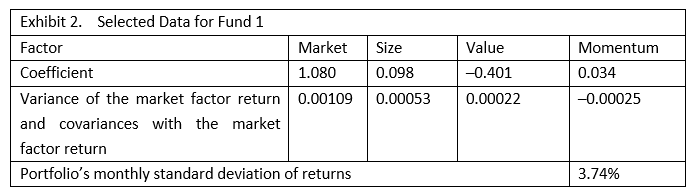

Based on Exhibit 2, the portion of total portfolio risk that is explained by the market factor in Fund 1’s existing portfolio is closest to:

选项:

A.3%

81%

87%

解释:

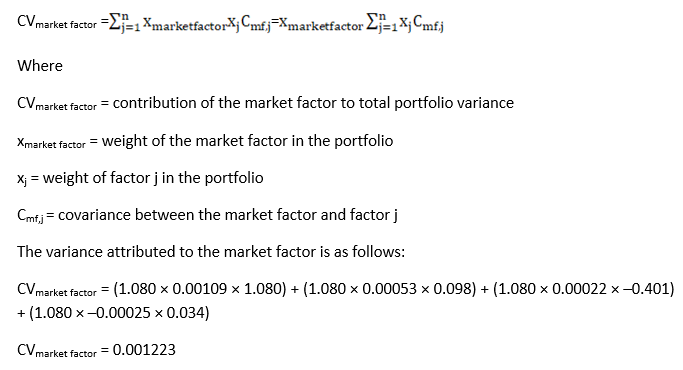

The portion of total portfolio risk explained by the market factor is calculated in two steps. The first step is to calculate the contribution of the market factor to total portfolio variance as follows:

The second step is to divide the resulting variance attributed to the market factor by the portfolio variance of returns, which is the square of the standard deviation of returns:

Portion of total portfolio risk explained by the market factor = 0.001223/(0.0374)2

Portion of total portfolio risk explained by the market factor = 87%

两个问题:

1.为什么coefficient可以直接作为权重weight, coefficient在统计学中应该是beta, 而beta=cov/(σm^2), 和weight还是有区别的,所以这里我不理解

2.最终结果算risk的占比或者说risk的贡献,什么情况下用方差相除,什么情况下用标准差相除?