NO.PZ2023040401000099

问题如下:

According to put–call–forward parity, if the put in a protective put with forward contract expires out of the money, the payoff is most likely equal to:

选项:

A.the market value of the underlying asset.

zero.

the face value of a risk-free bond.

解释:

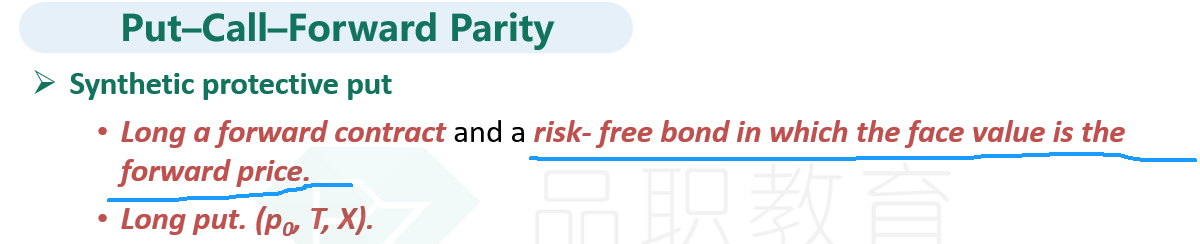

A protective put with forward contract is defined as a long position in (1) a bond that has the face value equal to the forward contract, (2) a forward contract, and (3) a long position in a put. If the put expires out of the money, the value of the overall position is equal to the market value of the asset.

+ F0(t) (payoff

of bond)

+ ST – F0(t)

(payoff of forward)

+ 0 (payoff of option)

= ST (payoff of strategy)

B is incorrect. Zero is the payoff of the put alone. This ignores the other positions in the strategy.

C is incorrect. The face value of the risk-free bond is the payoff of the protective put with forward contract if the put expires in the money.

如何判断C选项中的face value of the free bond指的是F0(T) 还是X? 加入put option 到期时in the money, payoff应该是X对么?