NO.PZ2023040501000035

问题如下:

Rowland turns his attention to the information provided about the company pension plan. The increasing pension costs combined with the impact on pension assets from poor investment performance had resulted in a funding deficit in the plan during 2014. In an attempt to better control pension costs Austell had made the following changes to the plan over the past two years:

During 2013 the company had changed the early retirement benefits for members who joined the plan before 2000.

During 2014 Austell capped the salary increases that were eligible for pensionable benefits to 1%.

Austell prepares its financial statements in accordance with International Financial Reporting Standards (IFRS) and has a December 31 year-end.

These changes were reported as plan amendments in the year made. Information concerning the company’s pension plan as of December 31, 2014 is shown in Exhibit 4. Rowland wanted to review the pension expense, cash flows and the plan’s funding position.

The benefits paid (in millions) from Austell’s pension plan in 2014 is closest to:

选项:

A.£74.0.

£55.0.

解释:

Benefits paid can be determined either from focusing on the change in pension plan assets or from the change in the benefit obligation over the year, as follows:

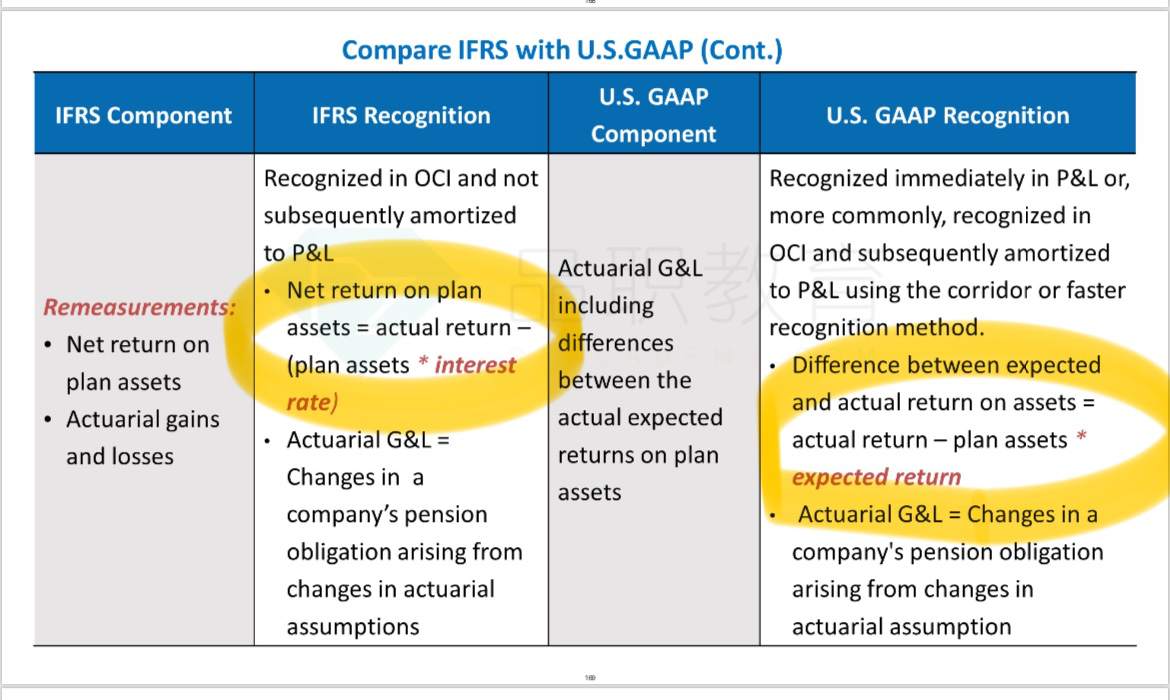

IFRS下:计入B/S asset的是fund status:plan asset - PBO

对于ending plan asset = beginnin asset + employor contribution + actual return on plan asset - benefit paid to employee

但是对于net interest expense = interest cost((PBO+PSC期初)*discount rate) - "E(r)"(FV of plan asset * discount rate),discount rate是国债或投资级公司债利率,这部分计入I/S

这就有了"E(r)"(FV of plan asset * discount rate)不等于actual return on plan asset的情况发生。

也就是说当"E(r)"(FV of plan asset * discount rate)< actual return on plan asset时:I/S中,计入费用的是"E(r)"(较小),而在B/S中,asset端增加了actual return on plan asset,equity端增加了"E(r)",asset的增加量大于equity的增加了,出现不匹配情况,这种情况如何调平?