NO.PZ2023010903000031

问题如下:

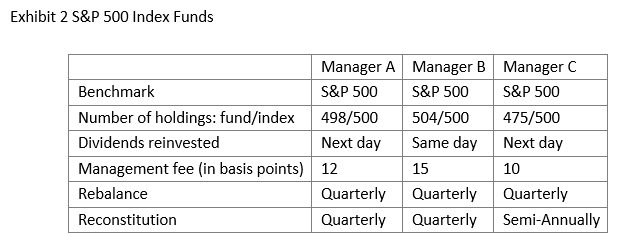

For the large-cap US equity portion of Sapphire’s investment portfolio, Cullen believes that there are some existing passive indexed-based funds that track the S&P 500 Index that the foundation should consider. Cullen presents Exhibit 2 to Sapphire’s board.

选项:

A.Manager A

Manager C

Manager B

解释:

Tracking error indicates how closely the portfolio behaves like its benchmark and measures a manager’s ability to replicate the benchmark return. Manager C is most likely to have the largest tracking error for three reasons:

l The portfolio contains a smaller number of the index holdings than the other two portfolios, resulting in a lower level of replication.

l Dividends are reinvested the day following receipt rather than the same day, which would cause cash drag relative to Manager B.

l The portfolio is reconstituted less frequently than the other two portfolios.

Although Manager C has a slightly lower management fee, which would result in a lower tracking error, the benefit is unlikely to offset the combined higher tracking error related to the other portfolio characteristics.

A and C are incorrect.

可是reconstitution的频率 以及 number of holdings对于tracking error的影响是一体两面的。

1.reconstitution frequency, 调仓越频繁,和benchmark越像,tracking error更小,但是调仓越频繁同时也会带来成本,成本越高,tracking error又会更大,所以不知道怎样判断

2.number of holding也是一样,数量越多,跟踪benchmark越好,tracking error越小,但是数量越多交易成本也越高,导致tracking error变大,所以不知道怎样判断