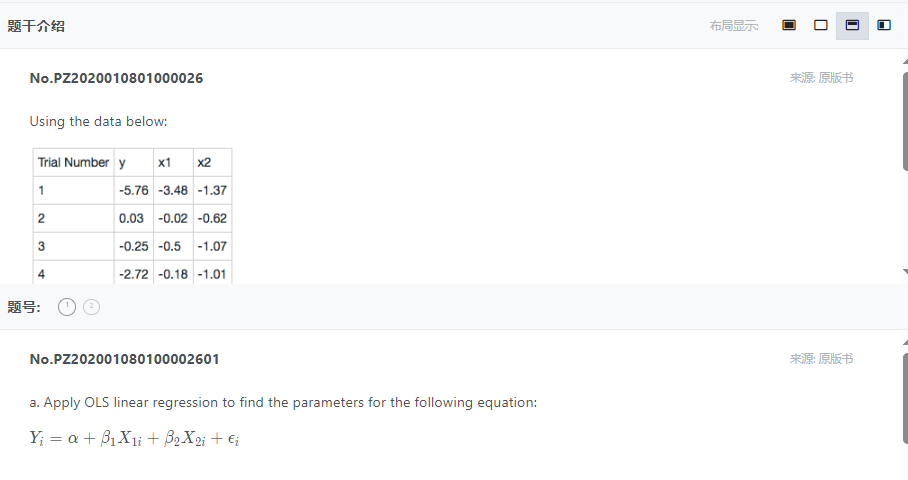

问题如下:

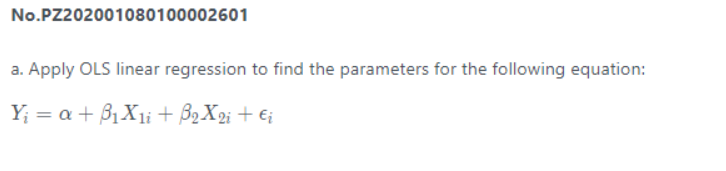

c. Using the results from part a and part b, and the correlation between the two explanatory variables, estimate the parameters for the full model:

Y=α+β1X1+β2X2

选项:

解释:

The key statement from the chapter is “the estimator β1 converges to β1+β2δ”

So, part a gives that:

β1+β2δ1=0

And part b gives that:

β2+β1δ2=−1.479

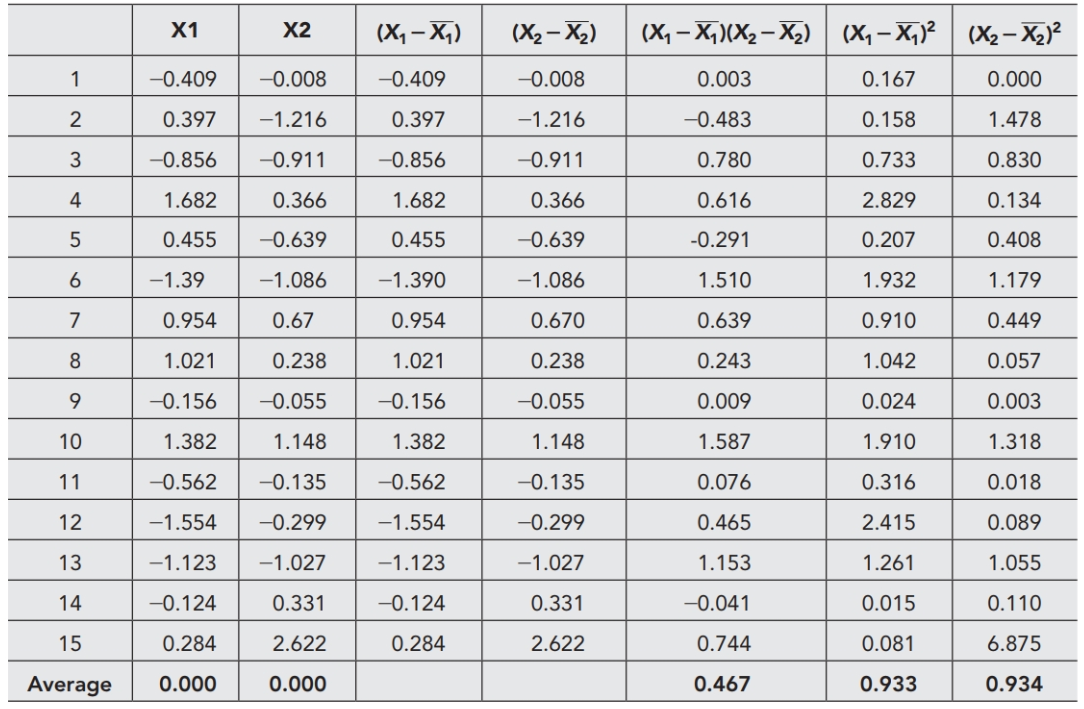

δ1=V[X1]Cov[X1,X2]=0.467/0.933=0.501

and

δ2=0.467/0.934=0.5

Note: In this case these quantities are essentially equal, but that will not usually be the case.

Plugging back in the 2 * 2 system of equations:

β1+0.501β2=0

β2+0.5β1=−1.479

Solving yields that

β1=0.989,β2=−1.9733

And plugging these back into the equation to find alpha:

Y=α+β1X1+β2X2=−2

Y=−2+0.989X1−1.9733X2