NO.PZ2024050101000095

问题如下:

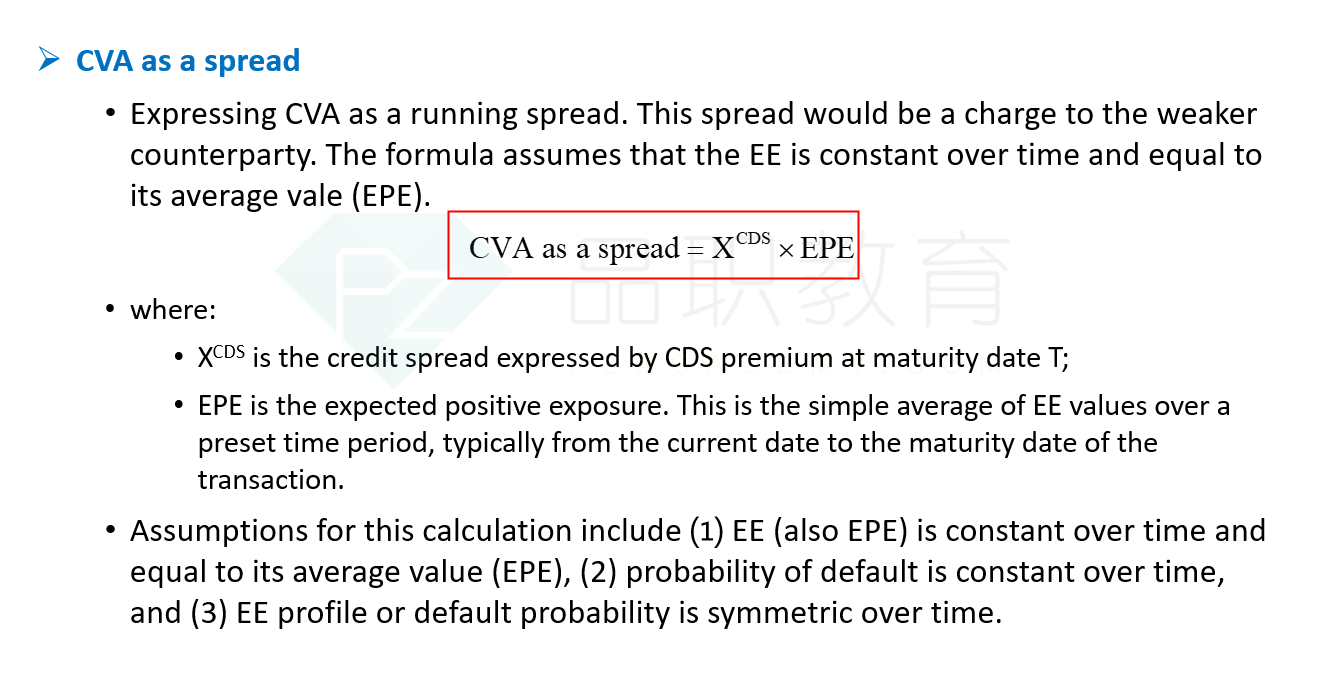

A bank enters into a swap agreement with a counterparty. The swap has no collateral requirements, and no netting agreements are present between the bank and the counterparty. The following data is available for the swap position:

• The counterparty expected exposure is 0.40% and approximately constant from month to month.

• The credit spread for a five year credit default swap on the counterparty is 500 bps.

• The counterparty’s probability of default within five years is 10%.

• The 5-year effective duration of the swap is 4.0.

Assuming no wrong-way risk on the position, which value is the closest approximation of the credit value adjustment expressed as a running spread?

选项:

A.2 bps

B.4 bps

C.5 bps

D.8 bps

解释:

请问为啥不是EAD*PD=0.4%*10%=4bp?