NO.PZ202207040100000306

问题如下:

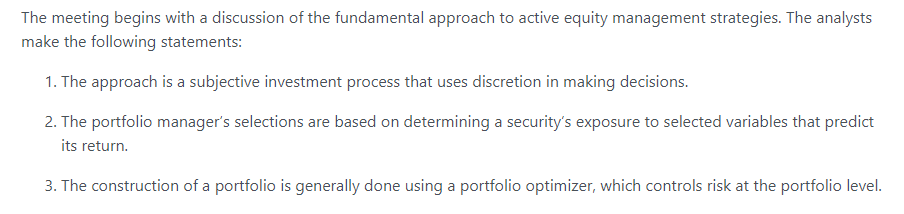

Which of the analysts’ statements regarding the fundamental approach is the most accurate?

选项:

A.

Statement 1

B.

Statement 2

C.

Statement 3

解释:

A is correct. Statement 1 is correct. The fundamental approach is a subjective investment process that uses discretion in making decisions.

B is incorrect. Statement 2 in incorrect. Determining a security’s exposure to selected variables that predict its return is a quantitative, not a fundamental, approach to active equity management.

C is incorrect. Statement 3 is incorrect. Using a portfolio optimizer to control the risk in the construction of a portfolio is a quantitative approach.

麻烦老师详细讲下b选项,谢谢