NO.PZ2020010801000033

问题如下:

What is the strongest justification for using OLS to estimate model parameters?

解释:

When the errors are iid normally distributed, then the OLS estimator of the regression parameters ( and , but not ) is an MVUE (Minimum Variance Unbiased Estimator), and so there is not a better estimator available.

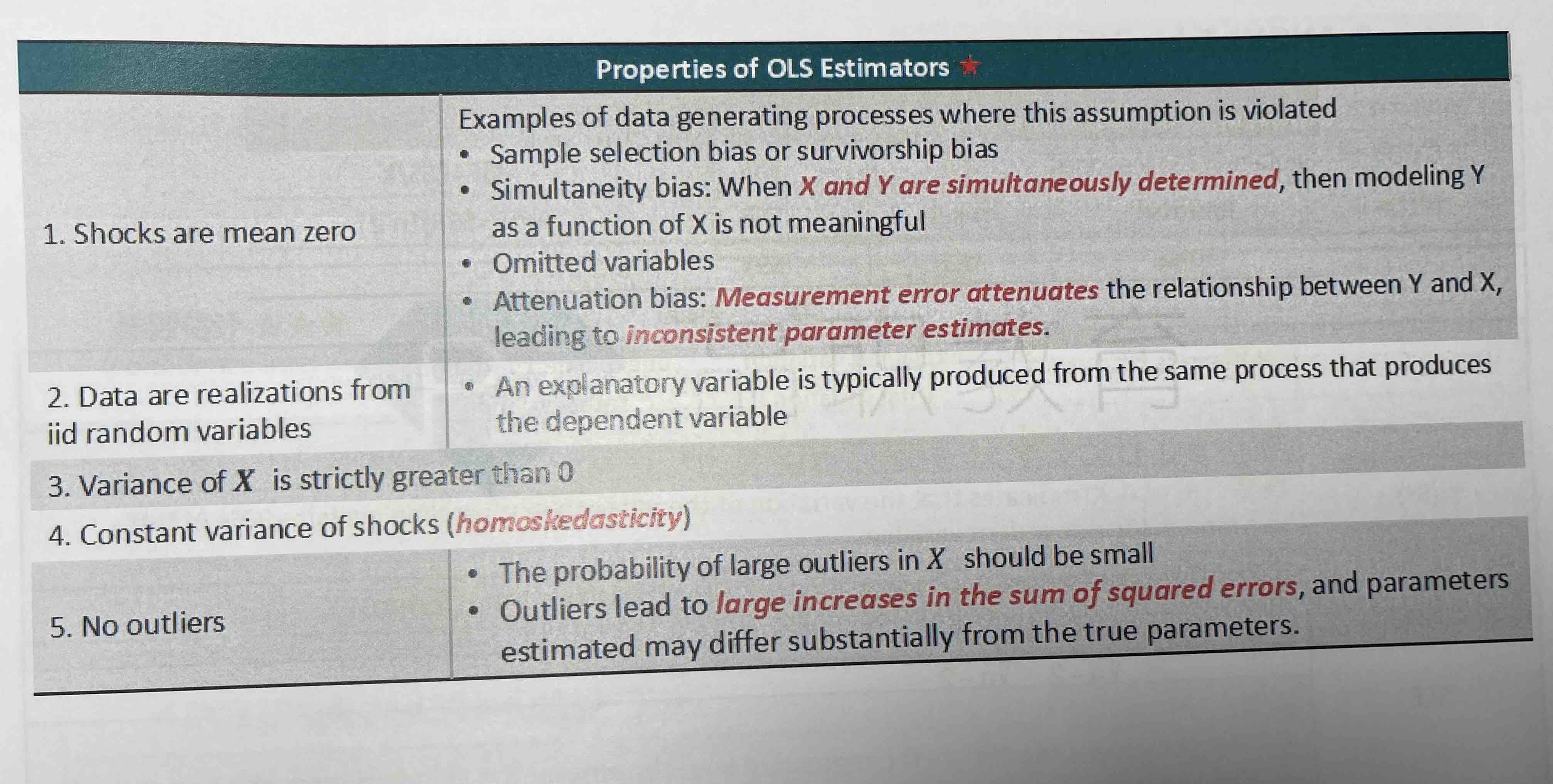

老师,在讲义里,没有提到OLS的前提是e独立同分步,且e服从正态分布呀,独立能理解但为什么要求e是同分步,且e服从正态分步呢?