NO.PZ202207040100000801

问题如下:

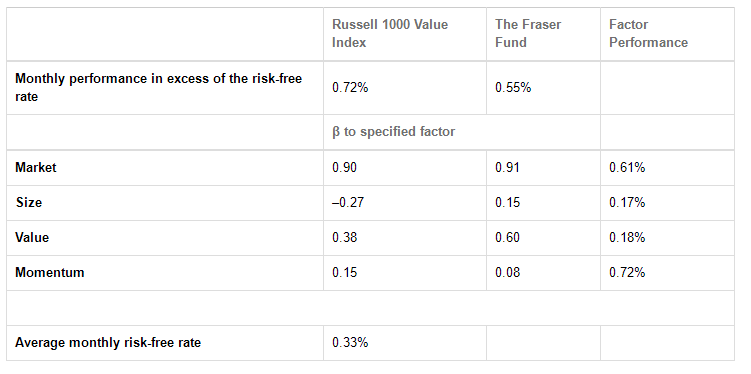

Using Exhibit 1, the average monthly return of the Fraser Fund that is unexplained by rewarded factors is closest to:选项:

A.–0.20%. B.–0.17%. C.0.13%.解释:

SolutionA is correct. Return from unrewarded factors = Actual monthly performance – Return from rewarded factors.“Alpha” = RA – ∑βpkFkwhere

RA = Actual portfolio performance

βpk = The sensitivity of the portfolio (p) to each rewarded factor (k)

Fk = The return for each rewarded factor

Return from rewarded factors = (0.91 × 0.61%) + (0.15 × 0.17%) + (0.60 × 0.18%) + (0.08 × 0.72%) = 0.75%.

“Alpha” = Return from unrewarded factors = 0.55% – 0.75% = –0.20%.

B is incorrect. This is the “active return”: Actual – Benchmark = 0.55% – 0.72% = –0.17%.

C is incorrect. This adds the risk-free return back to the rewarded factor return = 0.33% – 0.20% = 0.13%.

Actual monthly performance为什么不用0.55%加回risk-free rate?加回才是monthly performance啊,这样答案就是C