NO.PZ2024042601000016

问题如下:

A credit risk analyst at a bank is using the Merton’s model to estimate the probability of default (PD) of a non-dividend-paying company. The company’s debt consists of only long-term zero-coupon bonds. The analyst gathers the following information:

What is the PD of the company and a limitation of using the Merton model to predict default of the company?

选项:

A.The company’s PD is 3.03%, and a limitation of the Merton model is that it cannot be applied to debt holdings maturing in more than 1 year.

The company’s PD is 4.04, and a limitation of the Merton model is that it only applies under the assumption that the value of the firm is normally distributed.

The company’s PD is 5.20%, and a limitation of the Merton model is that it is costly, especially for smaller firms, to continuously calibrate PD on historical series of actual defaults.

The company’s PD is 12.49%, and a limitation of the Merton model is that it is not capable of continuously calibrating PD due to continually changing movements in interest rates and market prices.

解释:

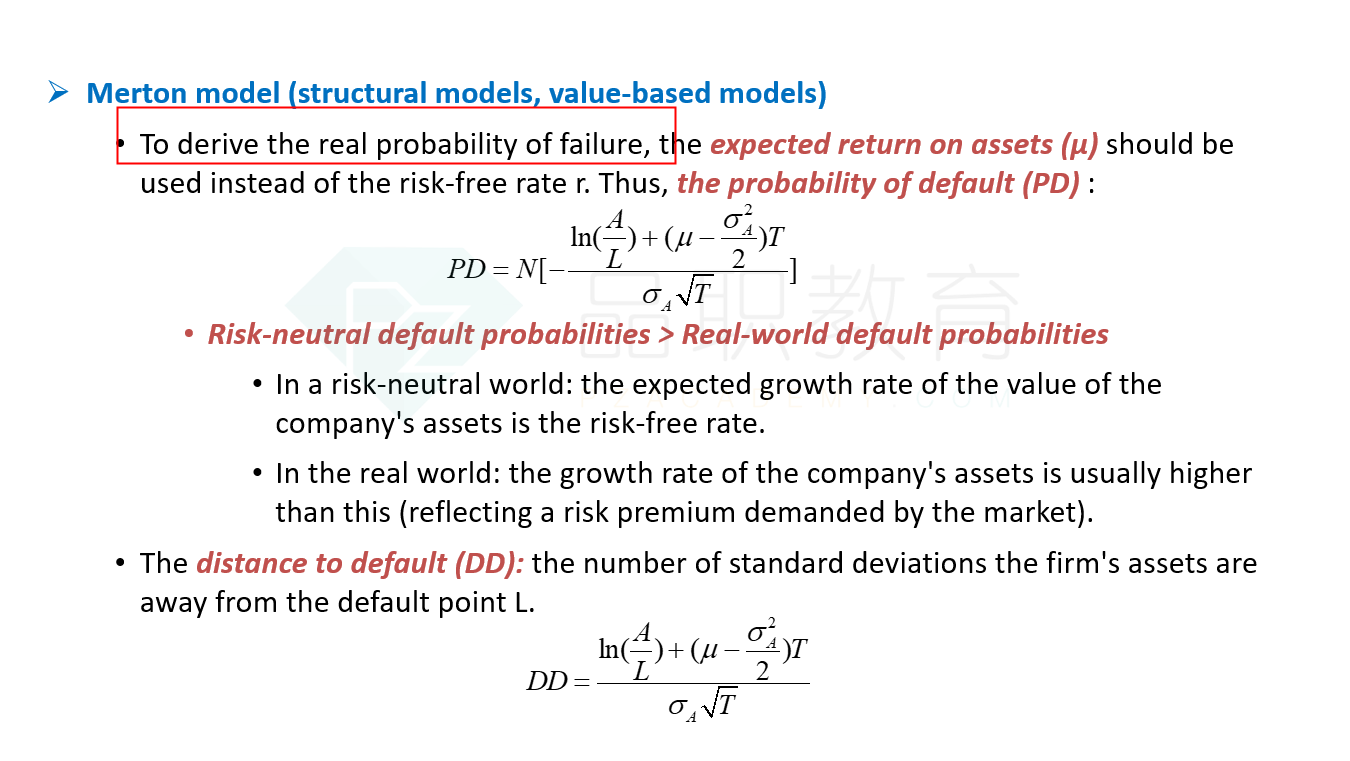

C is correct. Using the Merton model, the PD is expressed as follows:

V = CAD 400,000,000; F = CAD 300,000,000; volatility = 0.25; μ = 0.15; T- t = 1. Thus, the company’s PD = N(-1.626) = 5.20% (Using Excel: PD = NORMSDIST(-1.626) = 0.051975).

The Merton model has several limitations. It is applicable to liquid, publicly traded names only, and there is continuous need for calibration of the PD on historical series of actual defaults as an analytical requirement, a maintenance requirement, which is costly for smaller organizations. The Merton model also relies on the continually changing movements in market prices, volatility, and interest rates.

A is incorrect. 3.03% is the result obtained by subtracting (instead of adding) the last term in the numerator. The Merton model can be applied to debt holding maturing in more than 1 year.

B is incorrect. 4.04% is the result obtained by incorrectly adding the risk-free rate to the asset return in the term in the numerator of the PD formula. Also, the statement about a limitation of the Merton model that assumes the value of the firm is normally distributed is incorrect. The Merton model assumes the firm value is lognormally distributed.

D is incorrect. 12.49% is the result obtained by using the approximation formula to compute DtD = ((lnV – lnF) /σ) and deriving PD = N(-DtD). The Merton model involves (and is capable of) continuous calibration to account for the continually changing movements in market prices, volatility and interest rates, which is not a limitation.

根据公式,不是应该r(T-t)吗?r用无风险利率,题干中用3%,怎么变成μ?