NO.PZ2023120801000073

问题如下:

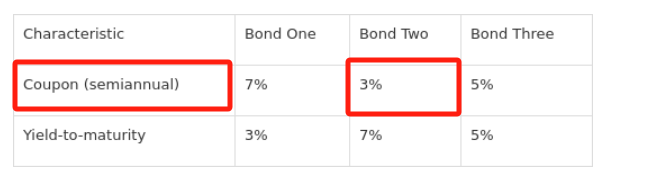

A portfolio manager is assessing the interest rate risk of three

bonds as she considers making an investment of USD50 million. All three bonds

are issued on 1 June 2026 and mature on 1 June 2030, and they have the

following characteristics:

The modified

duration for Bond Two is closest to:

选项:

A.3.59

B.3.65

C.3.78

解释:

Correct Answer: B

cash flow 为什么都是1.5?