NO.PZ2020010801000036

问题如下:

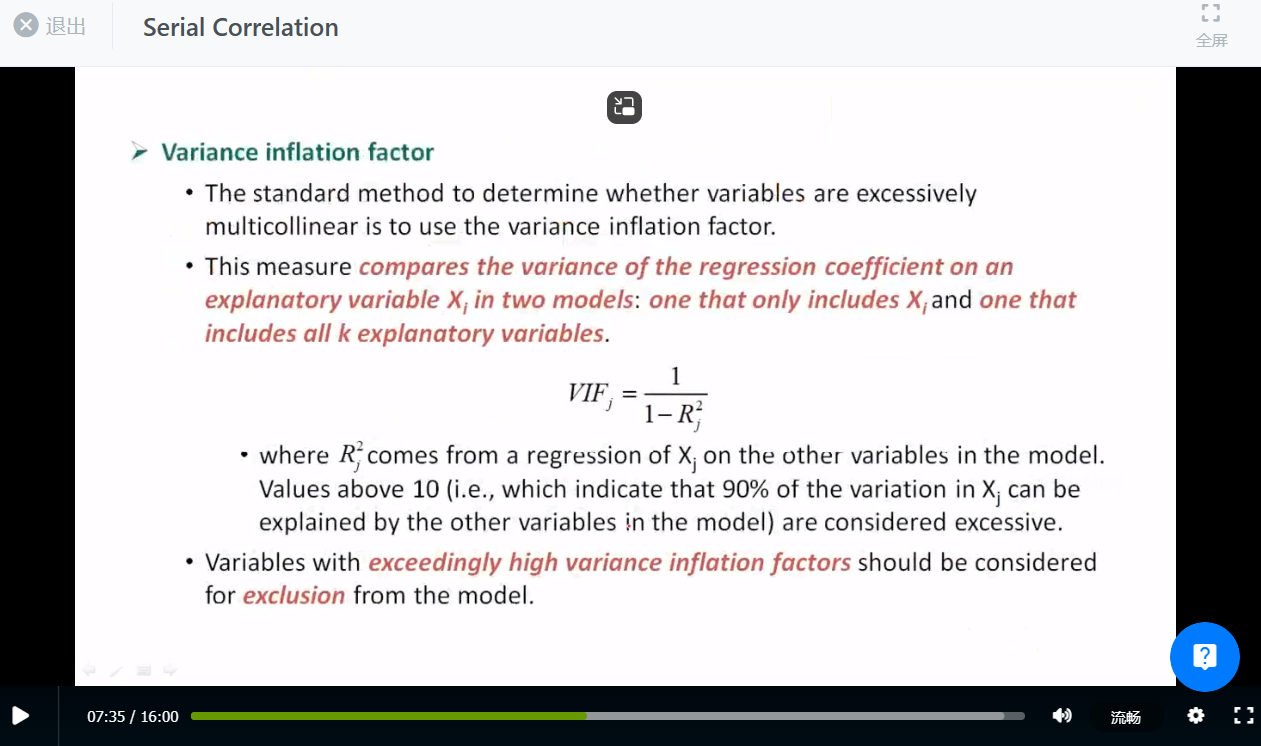

In a model with two explanatory variables, , what does the correlation need to be between the two regressors, X1 and X2, for the variance inflation factor to be above 10?

选项:

解释:

The variance inflation factor is , where measures how well variable j is explained by the other variables in the model. Here there are two variables, and so . The variance inflation factor of 10 solves , so that or .

Correlations greater than (in absolute value) would produce values above 10.

这个知识点在新考纲范围内吗