问题如下图:

选项:

A.

B.

C.

D.

解释:

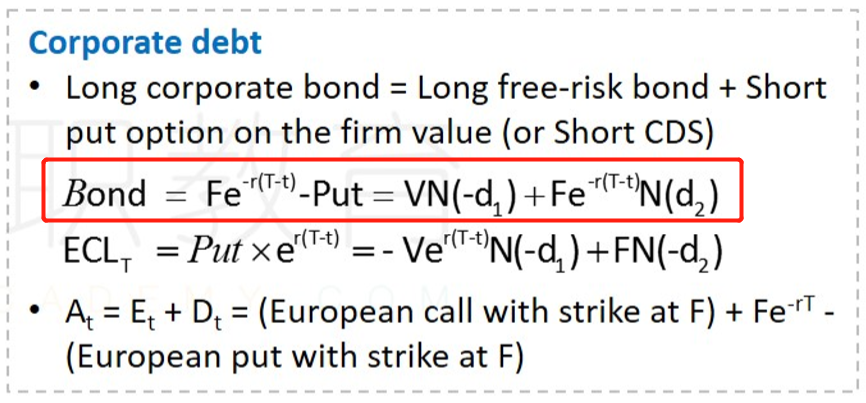

这里的debt value指的是risk free bond还是risky bond?

NO.PZ2016082406000039 Using the Merton mol, the value of the increases if all other parameters are fixeanI. The value of the firm creases. II. The riskless interest rate creases. III. Time to maturity increases. IV. The volatility of the firm value creases. I anII only I anIV only II anIII only II anIV only ANSWER: The value of cret-sensitive is B=Ke−(r+s)tB=Ke^{-(r+s)t}B=Ke−(r+s)t. This increases (1) if the risk-free interest rate creases, or (2) if the cret sprecreases, or (3) if the maturity creases. The cret sprecreases if the value of the firm goes up, or if the leverage goes wn, or if the volatility goes wn. Hence, the value of increases if the riskless rate creases or if the volatility creases. time to maturity 和 有关吗? 应该是客观认为存在吧。 是混淆象吧

NO.PZ2016082406000039 Using the Merton mol, the value of the increases if all other parameters are fixeanI. The value of the firm creases. II. The riskless interest rate creases. III. Time to maturity increases. IV. The volatility of the firm value creases. I anII only I anIV only II anIII only II anIV only ANSWER: The value of cret-sensitive is B=Ke−(r+s)tB=Ke^{-(r+s)t}B=Ke−(r+s)t. This increases (1) if the risk-free interest rate creases, or (2) if the cret sprecreases, or (3) if the maturity creases. The cret sprecreases if the value of the firm goes up, or if the leverage goes wn, or if the volatility goes wn. Hence, the value of increases if the riskless rate creases or if the volatility creases. 为什么volatility会影响Firm Value?

Using the Merton mol, the value of the increases if all other parameters are fixeanI. The value of the firm creases. II. The riskless interest rate creases. III. Time to maturity increases. IV. The volatility of the firm value creases. I anII only I anIV only II anIII only II anIV only ANSWER: The value of cret-sensitive is B=Ke−(r+s)tB=Ke^{-(r+s)t}B=Ke−(r+s)t. This increases (1) if the risk-free interest rate creases, or (2) if the cret sprecreases, or (3) if the maturity creases. The cret sprecreases if the value of the firm goes up, or if the leverage goes wn, or if the volatility goes wn. Hence, the value of increases if the riskless rate creases or if the volatility creases. 老师这个题具体从哪个知识点来解析,()只符合其中几个 我的想法是上升,V上升 1和2 都是下降的 3,4 都是上升的, 选不出来答案D

Using the Merton mol, the value of the increases if all other parameters are fixeanI. The value of the firm creases. II. The riskless interest rate creases. III. Time to maturity increases. IV. The volatility of the firm value creases. I anII only I anIV only II anIII only II anIV only ANSWER: The value of cret-sensitive is B=Ke−(r+s)tB=Ke^{-(r+s)t}B=Ke−(r+s)t. This increases (1) if the risk-free interest rate creases, or (2) if the cret sprecreases, or (3) if the maturity creases. The cret sprecreases if the value of the firm goes up, or if the leverage goes wn, or if the volatility goes wn. Hence, the value of increases if the riskless rate creases or if the volatility creases. 我不能理解(4)他说杠杆率下降,但是杠杆率等于A/E,当债务 上升的时候杠杆率应该是上升的,为什么杠杆率是下降的呢?

Using the Merton mol, the value of the increases if all other parameters are fixeanI. The value of the firm creases. II. The riskless interest rate creases. III. Time to maturity increases. IV. The volatility of the firm value creases. I anII only I anIV only II anIII only II anIV only ANSWER: The value of cret-sensitive is B=Ke−(r+s)tB=Ke^{-(r+s)t}B=Ke−(r+s)t. This increases (1) if the risk-free interest rate creases, or (2) if the cret sprecreases, or (3) if the maturity creases. The cret sprecreases if the value of the firm goes up, or if the leverage goes wn, or if the volatility goes wn. Hence, the value of increases if the riskless rate creases or if the volatility creases. B=Ke−(r+s)t 这个等式是指的啥啊