NO.PZ2023120801000097

问题如下:

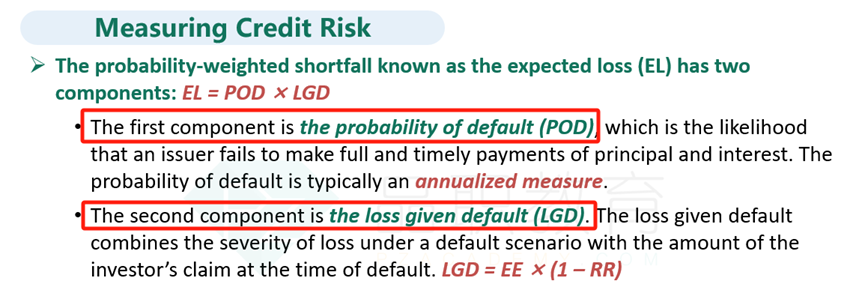

The two components of credit risk are default probability

and:

选项:

A.spread risk

loss severity

market liquidity risk

解释:

Correct Answer: B

The two components

of credit risk are default probability and loss severity. In the event of default,

loss severity is the portion of a bond’s value (including unpaid interest) an

investor loses. A and C are incorrect because spread and market liquidity risk

are credit-related risks, not components of credit risk.

我记得何老师说信用风险包括违约的风险和评级被下调的风险,评级被下调,不就是spread 变大吗