NO.PZ2023040601000009

问题如下:

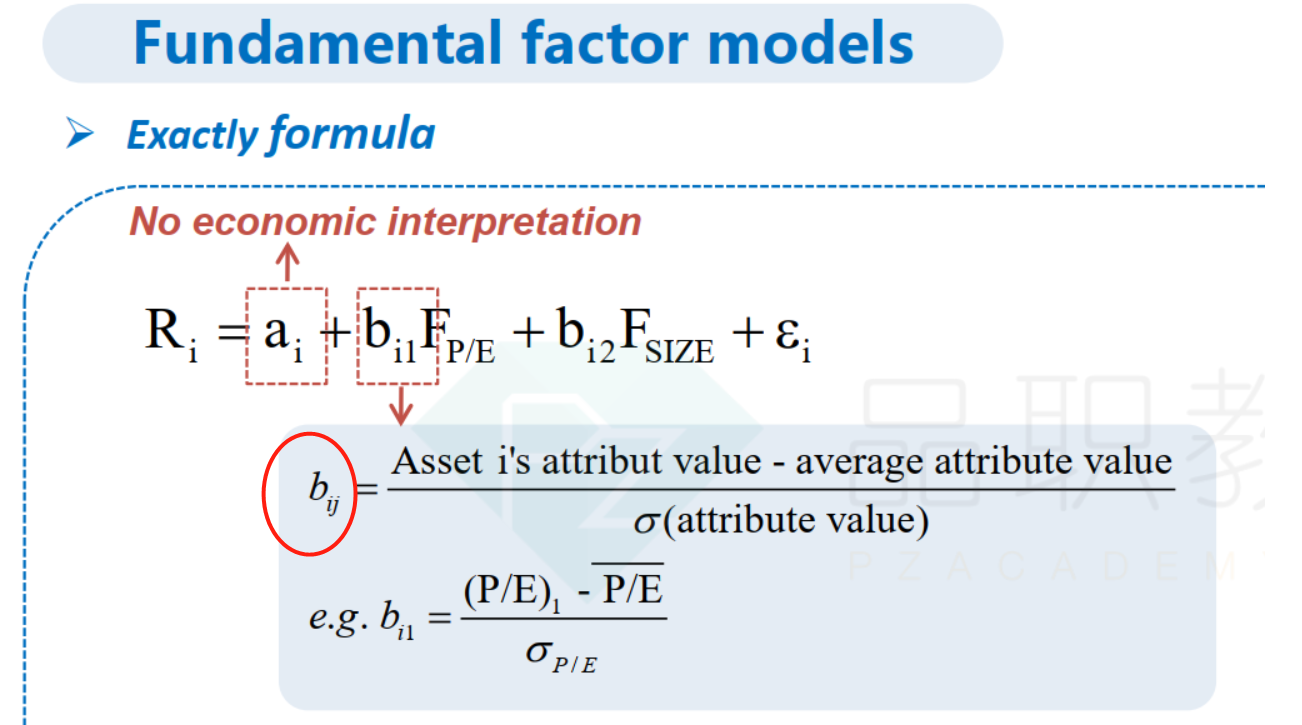

Yusuf states, “Multifactor models fall into one of three categories: macroeconomic factor models, fundamental factor models, and statistical factor models. For macroeconomic factor models, the factors are the value, or level, of selected macroeconomic variables. For fundamental factor models, the factors are company share attributes, such as price-to-earnings ratio and market capitalization. Finally, when using statistical factor models, we apply statistical techniques, such as factor analysis or principal component analysis, to derive factors that are portfolios of securities that best explain historical return covariances and variances.”

In her statement about the three types of multifactor models, Yusuf is least likely correct with respect to:

选项:

A.

statistical factor models.

B.

fundamental factor models.

C.

macroeconomic factor models.

解释:

C is correct. In macroeconomic models, the factors are “surprises” (how much higher or lower than what was expected) in macroeconomic variables, not the level or value of macroeconomic variables.

A is incorrect. Statistical models are described accurately. Statistical factor models use factor analysis to produce factors that are portfolios of securities that best explain historical return covariances. Alternatively, they use principal component analysis to derive factors that are portfolios of securities that best explain historical return variances.

B is incorrect. Fundamental factor models are described correctly; the factors are company share attributes, such as price-to-earnings ratio and market capitalization.

基本面的数据一般不是都要相对于行业平均,做些处理吗?