NO.PZ2023091802000069

问题如下:

You are examining the exchange rate between the U.S. dollar and the

Euro and have the following information:

Current USD/EUR exchange rate is 1.25.

Current USD-denominated 1-year risk-free interest rate is 4%

per year.

Current EUR-denominated 1-year risk-free interest rate is 7%

per year.

According to the interest rate parity theorem, what is the 1-year forward USD/EUR exchange rate?

选项:

A.

0.78

B.

0.82

C.

1.21

D.

1.29

解释:

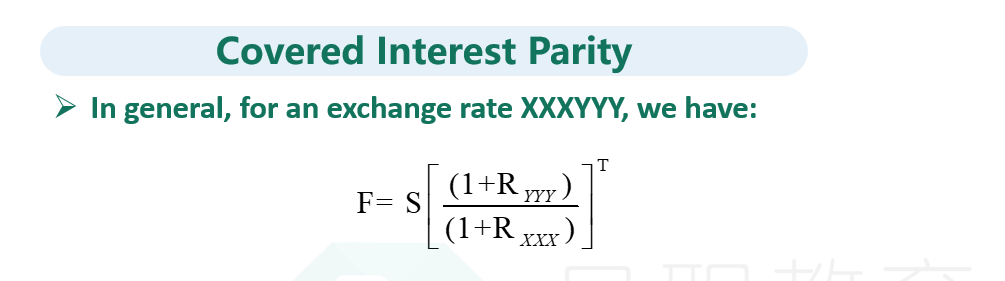

The forward rate, Ft, is given by the interest rate parity equation:

where S0 is the spot exchange rate, r is the domestic (USD) risk-free rate, and rf is the foreign (EUR) risk-free rate, t is the time to delivery.

Substituting the values in the equation:

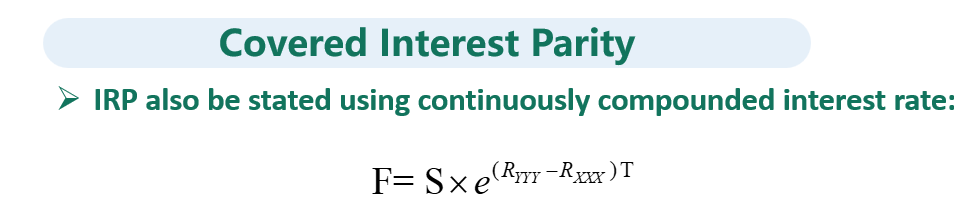

我记得老师明确说的是XXXYYY=FP 那么XXX=YYYFP 这道题正好反过来 还有讲义关于连续复利的公式是F=S✖️e的Rxxx-Ryyy✖️T