NO.PZ2023091802000079

问题如下:

The table below gives

coupon rates and mid-market price for three U.S. Treasury bonds for settlement

on (as of) May 31, 2013

Which of the following is nearest to the implied discount function (set of discount factors) assuming semi-annual compounding?

选项:

A.d(0.5) = 0.9370, d(1.0) = 0.8667, d(1.5) = 0.9210

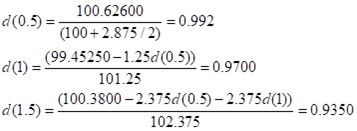

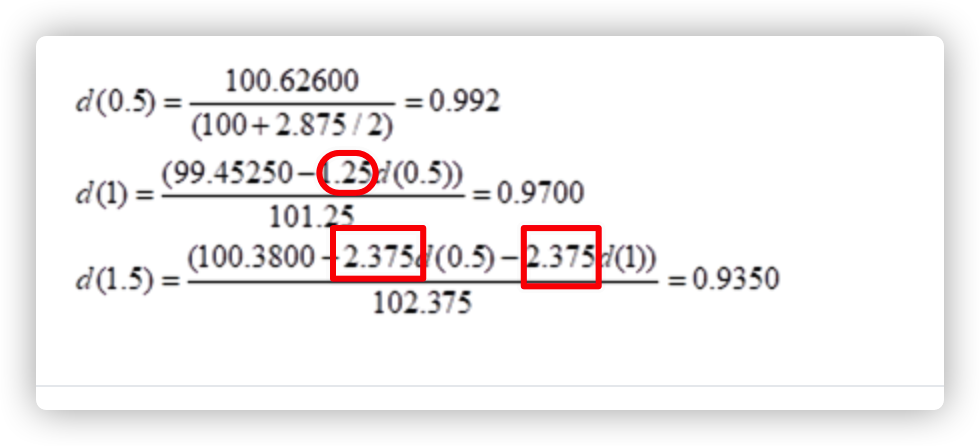

B.d(0.5) = 0.9920, d(1.0) = 0.9700, d(1.5) = 0.9350

C.d(0.5) = 0.9999, d(1.0) = 0.7455, d(1.5) = 0.8018

D.d(0.5) = 1.0350, d(1.0) = 1.1175, d(1.5) = 0.6487

解释:

The future value of $1 invested for time t is 1/d(t).