NO.PZ2023091802000070

问题如下:

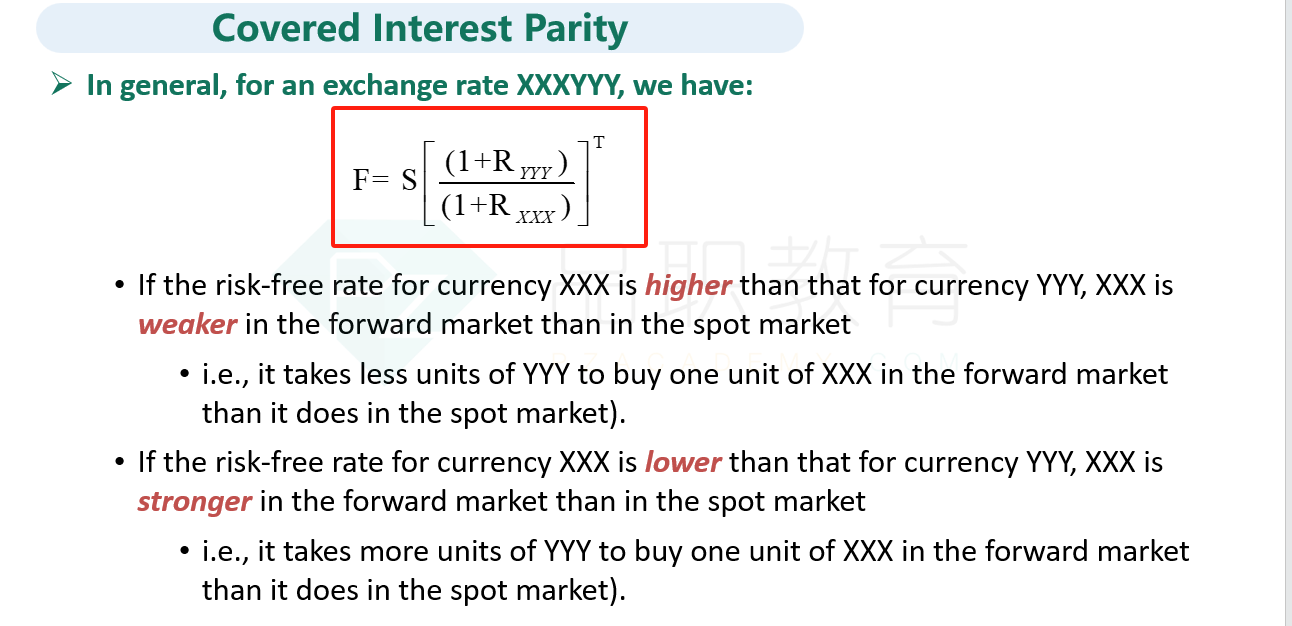

A trader was asked to determine the no-arbitrage 3-year forward exchange rate between the US dollar and the EUR. She observed that the current spot exchange rate between the US dollar and the EUR is USD 1.30 per EUR. She also checked with the chief economist of the bank and found that. in the US, the 3-year real risk-free interest rate is 1.00% and the expected inflation rate is 2.00%, while in the euro-zone, the 3-year real risk-free interest rate is 1.25% and the expected inflation rate is 2.50% Assuming that the real rates and inflation rates are compounded annually, the trader's best estimate of the 3-year forward exchange rate is closest to:

选项:

A.USD 1.15 per EUR.

B.USD 1.22 per EUR.

C.USD 1.27 per EUR.

D.USD 1.35 per EUR.

解释: