NO.PZ2023091701000032

问题如下:

A risk manager is exploring the interest rate sensitivity of an insurer’s bond portfolio and is considering a 2-year 6% coupon bond with a face value of USD 100.The coupon is paid annually, and the bond yield is 8% per year with annual compounding. What is the approximate dollar duration of the bond, where dollar duration is defined as the modified duration multiplied by the current value of the bond?

选项:

A.162

B.173

C.

180

D.187

E.187

解释:

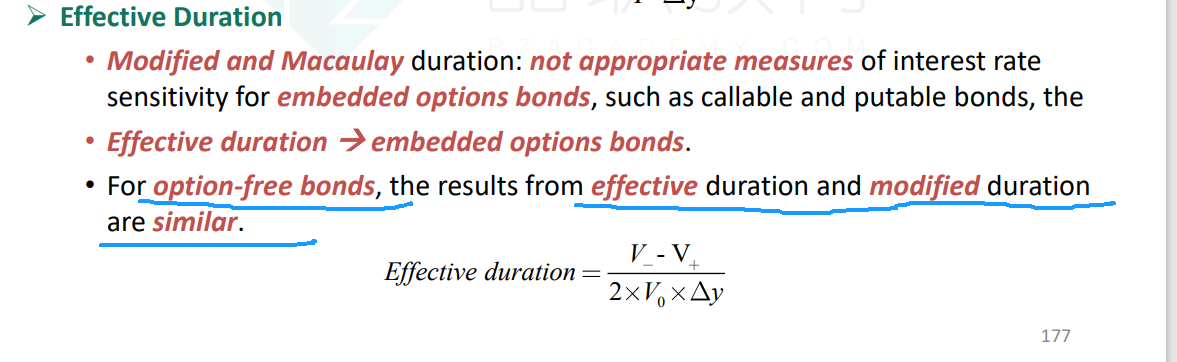

题中算出effective duration之后, 为什么没有换算modified duration 就直接计算dollar duration了?