NO.PZ2023021601000041

问题如下:

Which of the following portfolio performance measures are the most appropriate for an investor who holds a fully diversified portfolio?

选项:

A.Treynor ratio and Jensen's alpha.

B.M-Squared and Sharpe ratio.

C.Sharpe ratio and Treynor ratio.

解释:

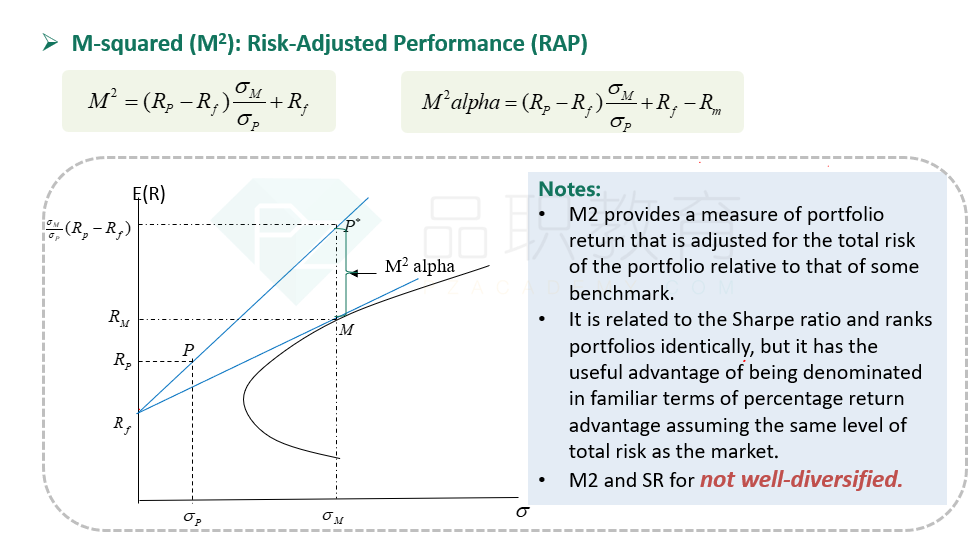

For an investor who holds a fully diversified portfolio, the Treynor ratio and Jensen's alpha are the appropriate portfolio performance measures. They are appropriate because in a fully diversified portfolio, only systematic risk matters; both these metrics measure performance relative to beta or systematic risk.M Squared请问一般用来做什么的?需要掌握计算吗