NO.PZ2023040401000082

问题如下:

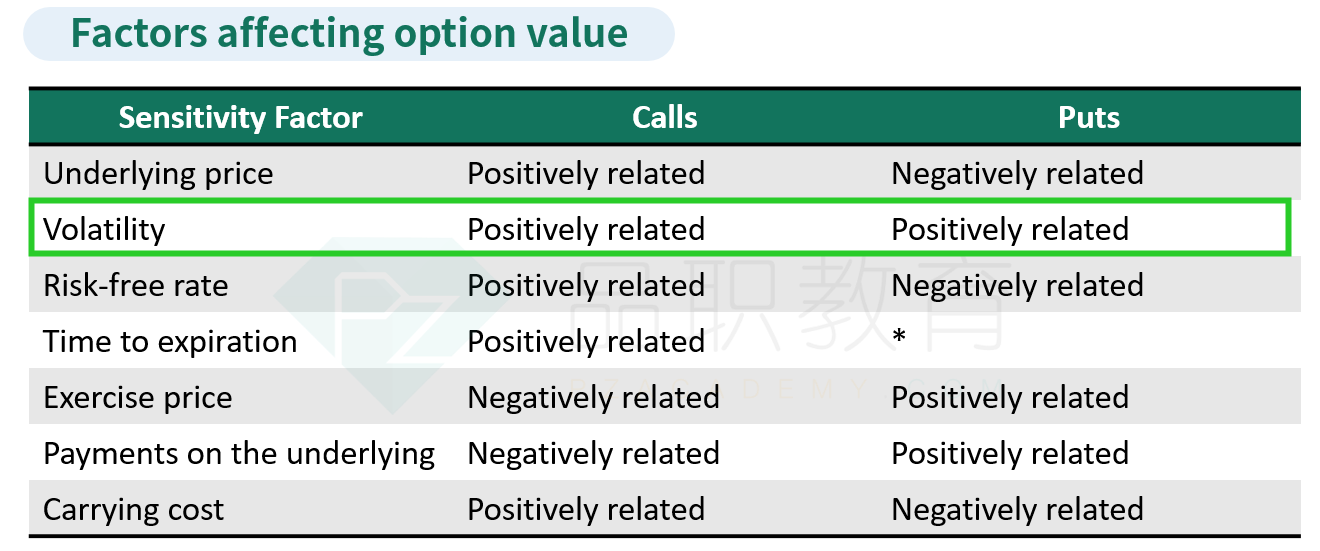

The value of a European call option is inversely related to the:

选项:

A.

exercise price.

B.

time to expiration.

C.volatility of the underlying.

解释:

A is correct. The value of a European call option is inversely related to the exercise price. A lower exercise price means there are more potential outcomes at which the call expires in-the-money. The option value will be greater the lower the exercise price. For a higher exercise price, the opposite is true. Both the time to expiration and the volatility of the underlying are directly (positively) related to the value of a European call option.

c怎么理解………..在公式有对应字母吗