NO.PZ2023091701000134

问题如下:

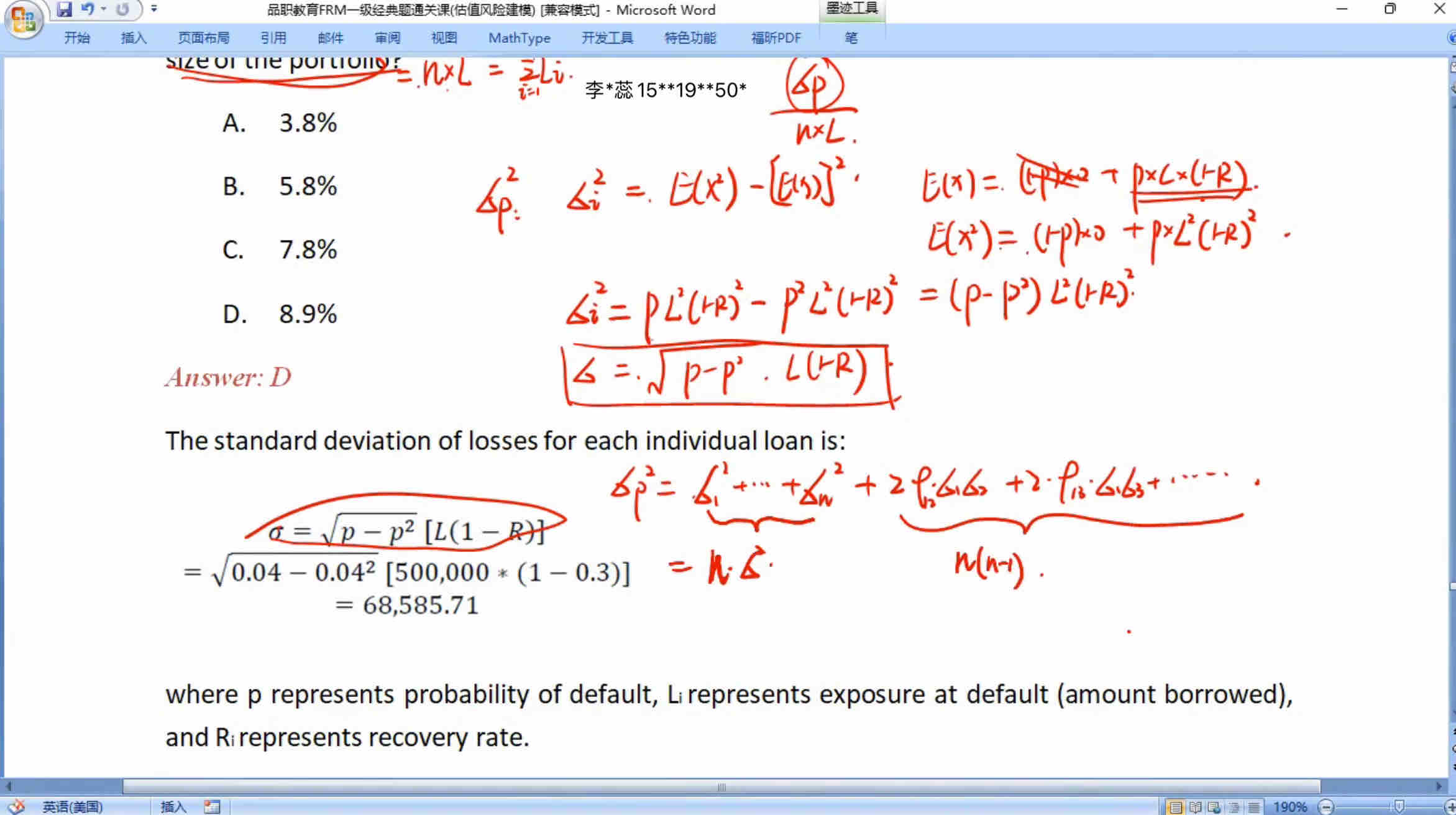

A risk analyst at a bank is estimating the

distribution of credit losses for a portfolio of 30 identical loan exposures.

The analyst assumes that the credit losses follow a binomial distribution. Each

loan has the following characteristics:

• Amount: SGD 500,000

• Probability of default: 4%

• Recovery rate: 30%

• Average pairwise default correlation: 0.4

What is the standard deviation of losses on the loan portfolio expressed as a percentage of the size of the portfolio?

选项:

A.3.8%

B.5.8%

C.7.8%

D.8.9%

解释:

The standard

deviation of losses for each individual loan is:

where p represents probability of default, Li represents exposure at default (amount borrowed), and Ri represents recovery rate.

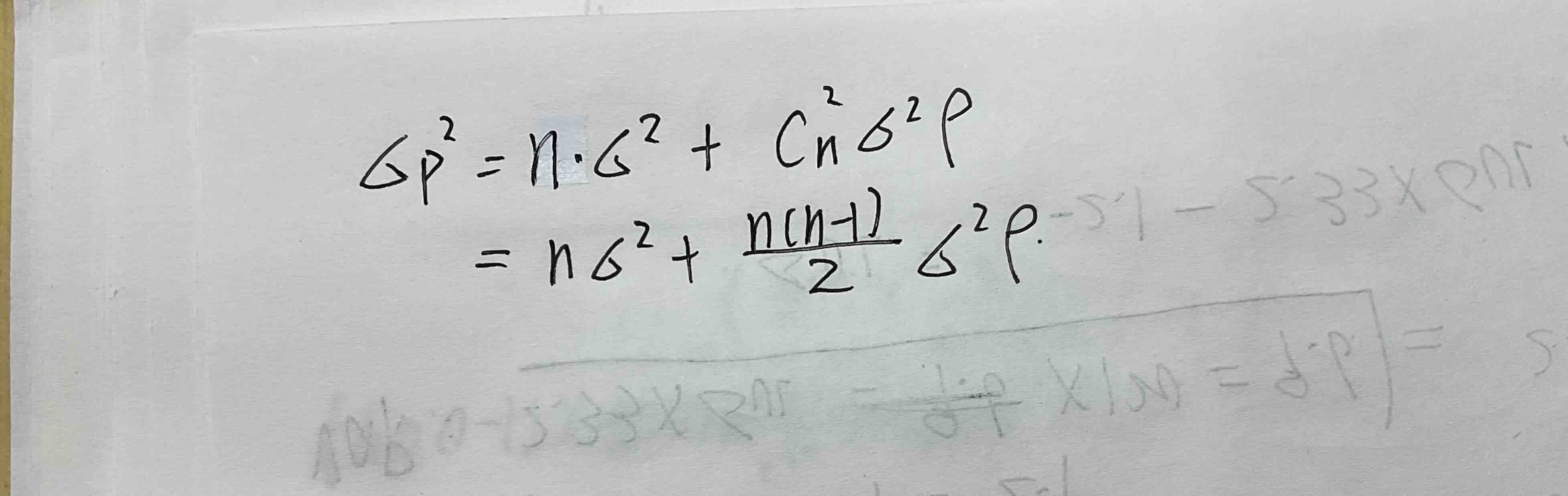

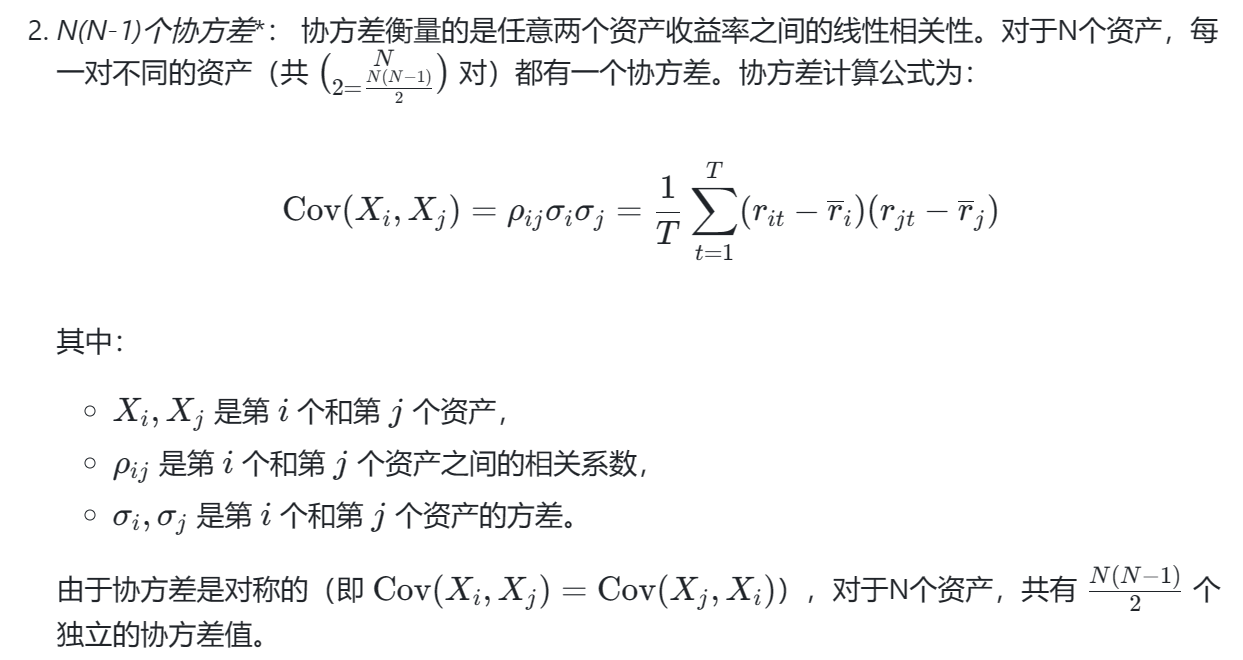

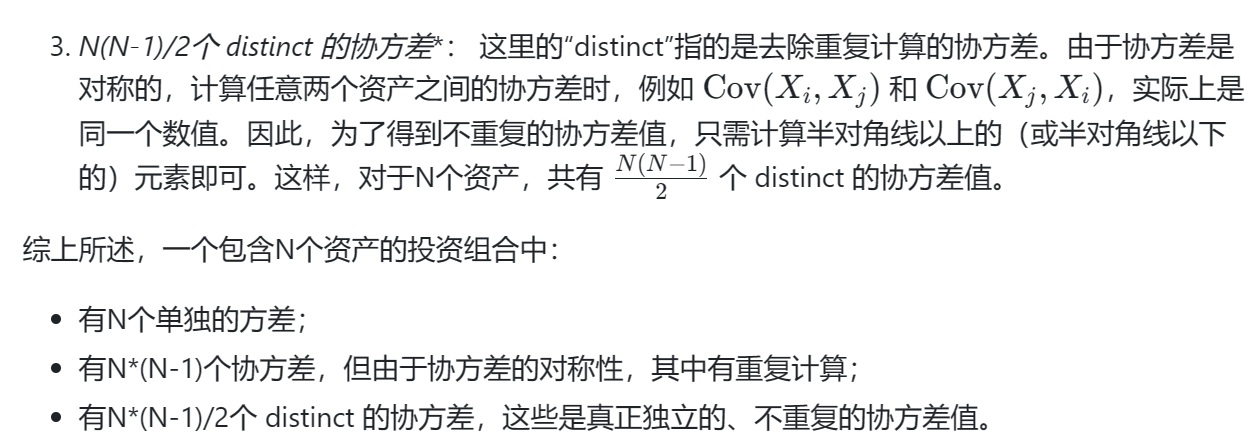

The standard deviation of losses on the portfolio of n loans as a percentage of its size is then calculated as:

视屏中解析求组合的标准差应该是: