NO.PZ2023091701000137

问题如下:

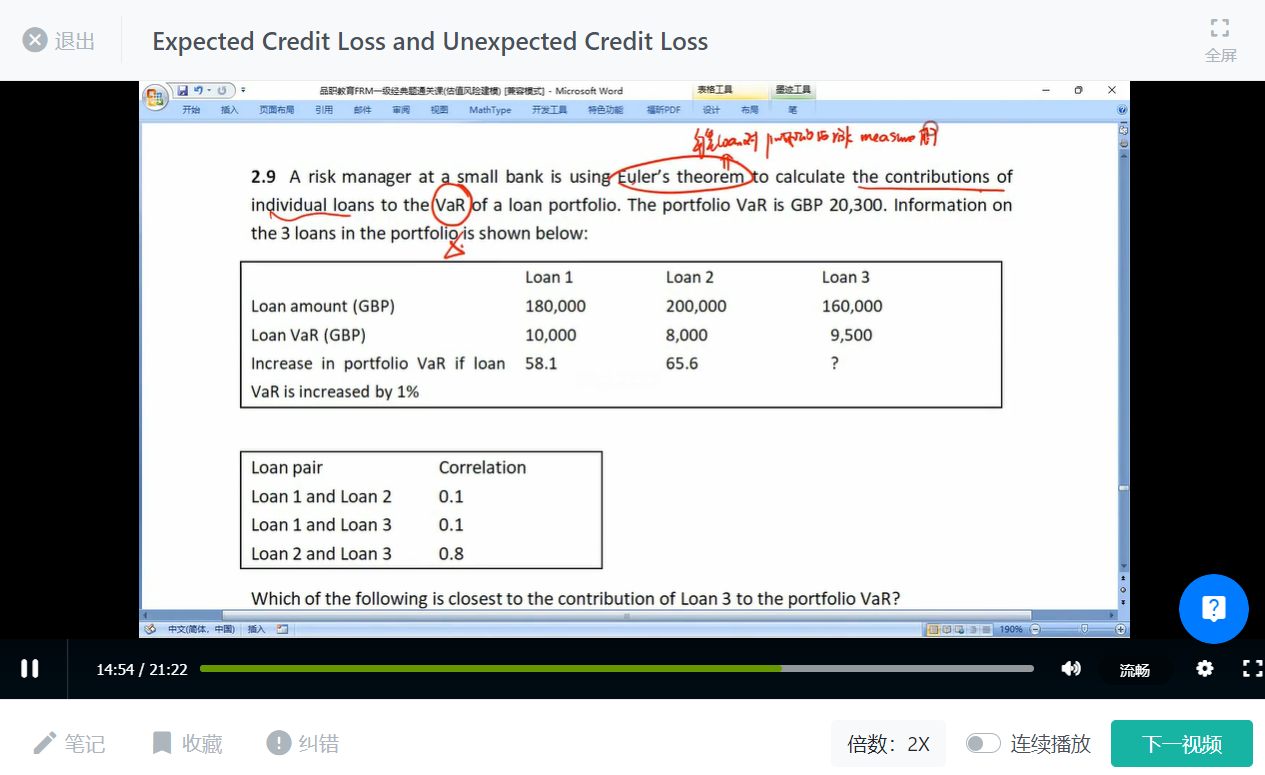

A risk manager at a small bank is using Euler’s theorem to calculate the contributions of individual loans to the VaR of a loan portfolio. The portfolio VaR is GBP 20,300. Information on the 3 loans in the portfolio is shown below:

Which of the following is closest to the contribution of Loan 3 to the portfolio VaR?

选项:

A.GBP 6,015 B.GBP 6,320 C.GBP 7,013

D.GBP 7,930

解释:

D is correct. In its application to credit risk, Euler’s theorem states that:

and that (in the

limit, as Δxigoes to zero):

where F is a (homogeneous) risk measure for a portfolio, xi is the same risk measure calculated for one component position in the portfolio, Δxi is a small change in this risk measure, and ΔFi is the resultant change in the portfolio’s risk measure.

Therefore, using the information given: