NO.PZ2023091701000132

问题如下:

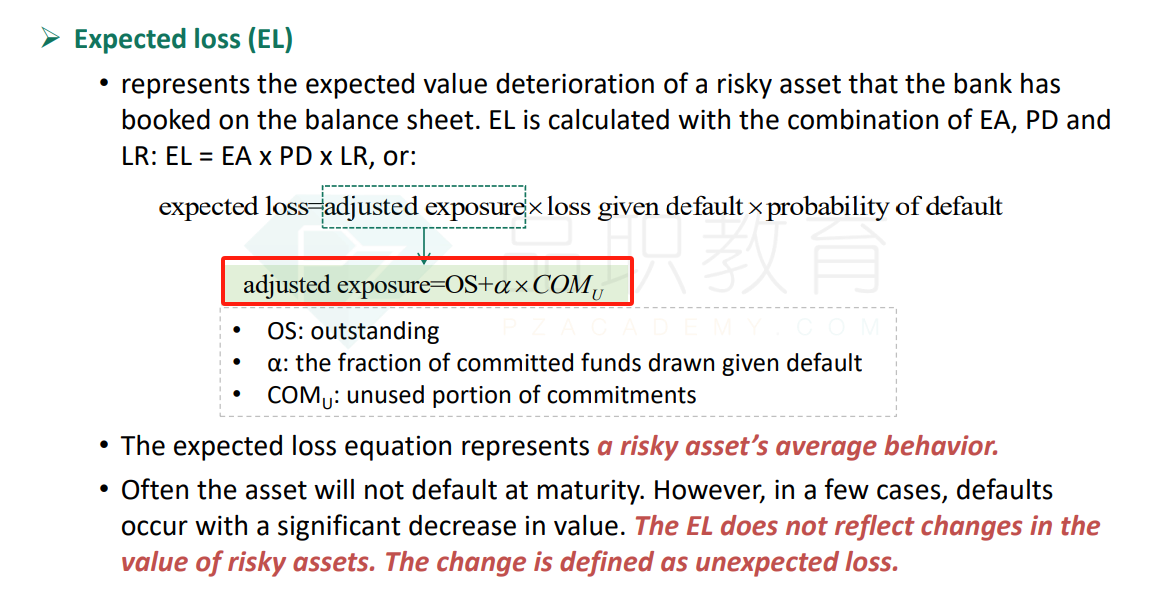

Suppose ABC bank has booked a loan with following characteristics, it has total commitment of 3,000,000, outstanding is 2,000,000. The bank estimates 1% default probability (EDF) in one year, and draw down on default is 65%. The bank is currently experienced 60% of loss given default. The standard deviation of EDF and LGD is 5% and 30%, respectively. Please find the adjusted exposure.

选项:

A.2,350,000 B.2,650,000 C.3,000,000 D.3,300,000解释: